phone

+91-9266032777

email

CaShiwalidagar@gmail.com

🏠 Section 50C – Stamp Duty Valuation & Capital Gains Tax (2026 Guide)

🏠 Section 50C – Stamp Duty Valuation & Capital Gains Tax (2026 Guide)

When selling property, many taxpayers are surprised to learn that capital gains tax may be calculated on a value higher than the actual sale price.

This happens due to Section 50C of the Income Tax Act.

If stamp duty valuation exceeds your sale consideration, tax authorities may adopt the higher value for capital gains computation.

This guide explains Section 50C rules clearly for property sellers in 2026.

📍 Capital Gains Advisory – South Delhi

📞 CA Shiwali – 9266032777

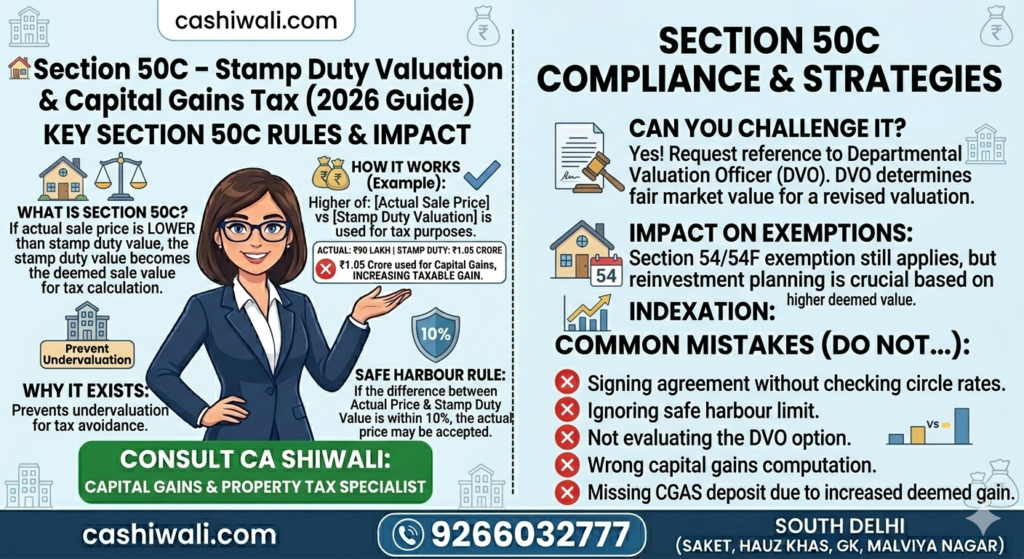

What is Section 50C?

Section 50C provides that:

If the sale consideration of immovable property is lower than the value adopted for stamp duty purposes, the stamp duty value may be considered as the deemed sale value for capital gains calculation.

In simple terms:

Higher of:

Actual sale price

Stamp duty valuation

May be used for tax purposes.

Why Does Section 50C Exist?

The provision was introduced to prevent undervaluation of property transactions for tax avoidance.

However, it can sometimes create genuine hardship where market conditions differ from circle rates.

10% Safe Harbour Rule

Currently, if the difference between:

Actual sale price

andStamp duty value

is within 10%, then actual sale price may be accepted.

If the difference exceeds 10%, Section 50C may trigger higher tax computation.

This is very important in fluctuating real estate markets.

Example – Section 50C Impact

Actual sale price: ₹90 lakh

Stamp duty value: ₹1.05 crore

If difference exceeds permitted limit, ₹1.05 crore may be considered for capital gains.

This increases taxable gain significantly.

Proper planning before agreement signing is advisable.

Can You Challenge Stamp Duty Value?

Yes.

If you believe stamp duty value exceeds fair market value:

You can request reference to a Departmental Valuation Officer (DVO)

DVO determines fair market value

Revised valuation may be adopted

However, this requires proper documentation and representation.

Does Section 50C Apply to All Property?

Section 50C applies to:

Land

Building

Both

It applies to capital assets (not stock-in-trade).

For builders and developers, Section 43CA may apply instead.

Section 50C and Indexation

If higher stamp duty value is adopted:

That value becomes sale consideration

Indexation is applied on cost side as usual

Section 50C and Section 54 Exemption

Even if Section 50C increases sale consideration:

Section 54 exemption can still be claimed

Reinvestment planning becomes more important

Common Mistakes in Section 50C Cases

❌ Signing agreement without checking circle rate

❌ Ignoring safe harbour limit

❌ Not evaluating DVO option

❌ Wrong capital gains computation

❌ Missing CGAS deposit due to increased deemed gain

Advance advisory is highly recommended before property registration.

FAQs – Section 50C

1. Is Section 50C applicable to inherited property?

Yes, if inherited property is sold below stamp duty value, Section 50C may apply.

2. Does 10% difference automatically avoid Section 50C?

If difference is within prescribed tolerance limit, actual sale price may be accepted.

3. Can Section 50C increase my tax liability?

Yes, because capital gains may be calculated on higher deemed value.

4. Can stamp duty value be challenged?

Yes, reference to DVO can be requested under prescribed procedure.

Capital Gains & Property Tax Advisory in South Delhi

For complete property tax planning including:

Section 50C adjustments

Read our detailed Capital Gains & Property Advisory Guide.

📞 9266032777

CA Shiwali – Property Tax & Capital Gains Consultant for Residents/NRI

South Delhi