phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Section 50C Stamp Duty Impact Calculator (India)

Calculate Capital Gains Impact of Stamp Duty Value

Use this calculator to estimate how Section 50C of the Income Tax Act affects the capital gains calculation when selling land or property.

Under Section 50C, if the stamp duty value of the property is higher than the actual sale price, the stamp duty value may be treated as the sale consideration for capital gains calculation.

This rule can increase the taxable capital gain even if the property was sold at a lower price.

Section 50C Stamp Duty Impact Calculator

Section 50C Stamp Duty Impact Calculator – Complete Guide

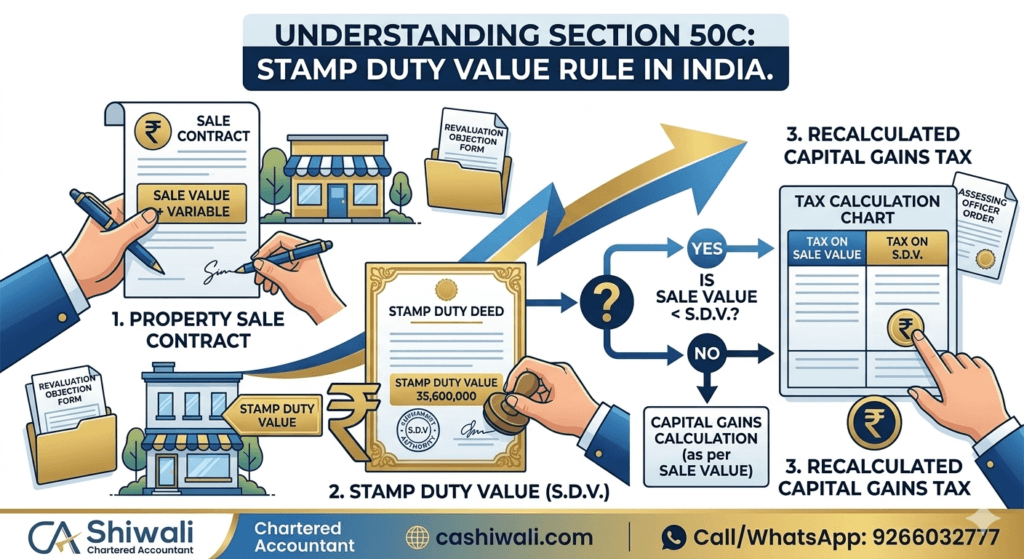

When selling property in India, many taxpayers assume that capital gains tax will be calculated based on the actual sale price mentioned in the sale deed. However, the Income Tax Act contains special provisions that may override the declared sale value. One of the most important rules in this regard is Section 50C of the Income Tax Act.

Section 50C states that if the stamp duty value of a property is higher than the actual sale price, the stamp duty value may be treated as the deemed sale consideration for calculating capital gains tax.

This rule was introduced to prevent undervaluation of property transactions and ensure that property sales reflect realistic market values for taxation purposes.

Our Section 50C Stamp Duty Impact Calculator helps taxpayers quickly estimate how this rule may affect their capital gains tax liability when selling land, plots, or other immovable property.

What is Section 50C of the Income Tax Act?

Section 50C is a special provision applicable to transfer of land or building.

If the sale consideration declared in the property transaction is lower than the stamp duty valuation adopted by the state government, the Income Tax Department may consider the stamp duty value as the sale price for capital gains calculation.

For example:

Actual sale price of property: ₹60,00,000

Stamp duty value determined by authority: ₹75,00,000

In this situation, capital gains tax may be calculated using ₹75,00,000 as the sale value, even though the seller actually received only ₹60,00,000.

This difference can significantly increase the taxable capital gain.

Why Section 50C Exists

Property transactions in India have historically involved underreporting of sale value to reduce stamp duty and tax liability. To discourage such practices, the government introduced Section 50C.

The objective of the provision is to:

Prevent undervaluation of property transactions

Ensure proper reporting of sale consideration

Protect government revenue from property taxes

By linking income tax calculations to stamp duty valuation, the law ensures that taxpayers cannot easily report a lower value to reduce capital gains tax.

How the Section 50C Calculator Works

The Section 50C Stamp Duty Impact Calculator works by comparing two values:

Actual sale price of property

Stamp duty value determined by the registrar

The calculator then applies the rule that the higher value is considered as the deemed sale consideration for calculating capital gains.

The formula used is:

Deemed Sale Value = Higher of (Actual Sale Price, Stamp Duty Value)

Capital Gain = Deemed Sale Value − Indexed Cost of Acquisition

If the stamp duty value is significantly higher than the sale price, the taxable capital gain increases accordingly.

Example of Section 50C Impact

Let’s understand this rule through a practical example.

Suppose a taxpayer sells a plot of land with the following details:

Actual sale price: ₹50,00,000

Stamp duty value: ₹65,00,000

Indexed cost of acquisition: ₹30,00,000

Since the stamp duty value is higher than the sale price, the Income Tax Act treats ₹65,00,000 as the sale consideration.

Capital gain calculation:

Deemed sale value: ₹65,00,000

Less: Indexed cost: ₹30,00,000

Capital gain = ₹35,00,000

Even though the taxpayer received only ₹50,00,000, the capital gain is calculated based on ₹65,00,000 due to Section 50C.

Safe Harbour Rule Under Section 50C

To provide relief in cases where the difference between sale price and stamp duty value is small, the government introduced a tolerance limit (safe harbour rule).

Currently, if the stamp duty value does not exceed 110% of the actual sale consideration, Section 50C may not apply.

Example:

Actual sale price: ₹50,00,000

Stamp duty value: ₹54,00,000

Since the difference is within the 10% safe harbour limit, the actual sale price may be accepted for capital gains calculation.

This provision helps reduce unnecessary tax disputes where valuation differences are minor.

What If Stamp Duty Value is Incorrect?

Sometimes the stamp duty authority may assign a value that is significantly higher than the actual market price.

In such cases, the taxpayer has the right to challenge the valuation.

The Income Tax Officer may refer the property valuation to a Departmental Valuation Officer (DVO) for independent assessment.

If the DVO determines a lower value, that valuation may be used for capital gains calculation instead of the original stamp duty value.

Capital Gains Planning for Property Sellers

Selling property can lead to substantial capital gains tax liability. However, the Income Tax Act provides certain exemptions that can help reduce or eliminate this tax.

For example:

If the capital gain arises from sale of a residential house, the taxpayer may claim exemption under Section 54 of the Income Tax Act.

If the capital gain arises from sale of land or other assets and the sale proceeds are invested in a new residential house, exemption may be available under Section 54F of the Income Tax Act.

Taxpayers can also temporarily park capital gains in the Capital Gains Account Scheme if they need additional time to invest in a new property.

Proper planning before selling property can significantly reduce the final tax burden.

Related Capital Gains Tools

To help taxpayers plan property transactions better, you can also use the following calculators on our website:

These tools can help you estimate tax liability, evaluate exemption eligibility, and plan investments effectively.

Frequently Asked Questions (FAQs)

What is Section 50C in income tax?

Section 50C is a provision that applies when land or building is sold at a price lower than the stamp duty value. In such cases, the stamp duty value may be treated as the sale consideration for capital gains tax calculation.

Does Section 50C apply to all property sales?

Section 50C applies specifically to transfer of land or building. It does not apply to sale of movable assets such as shares, mutual funds, or gold.

What is the 10% safe harbour rule under Section 50C?

If the stamp duty value is within 110% of the actual sale consideration, the actual sale price may still be accepted for capital gains calculation.

Can I challenge the stamp duty valuation?

Yes. If the stamp duty value is significantly higher than the actual market value, the taxpayer can request a reference to a Departmental Valuation Officer (DVO) for reassessment.

How can a Section 50C calculator help?

A Section 50C calculator helps estimate:

Deemed sale consideration

Capital gain after stamp duty adjustment

Potential tax liability

This allows property sellers to understand the tax impact before completing the transaction.

Need Help With Capital Gains on Property Sale?

Capital gains tax rules related to property transactions can be complex, especially when provisions like Section 50C, indexation, and exemption rules apply.

If you are planning to sell property or need assistance with capital gains tax planning, professional advice can help ensure proper compliance while minimizing tax liability.

CA Shiwali

Chartered Accountant – Capital Gains & Property Tax Advisory

🌐 Website: cashiwali.com

📞 Call / WhatsApp: 9266032777

Professional guidance can help you structure property transactions efficiently and avoid unexpected tax liabilities.