When calculating capital gains tax on property, determining the correct Fair Market Value (FMV) is extremely important. This is especially relevant when the property was purchased before 1 April 2001 or when the tax authorities require valuation verification.

Many property owners are confused about whether the FMV must be determined by a registered valuer or by a Chartered Accountant.

Understanding the difference between these professionals can help ensure that the capital gains calculation is accurate and compliant with income tax regulations.

This guide explains the role of a registered valuer and a Chartered Accountant in property valuation and capital gains tax planning.

What is Fair Market Value (FMV)?

Fair Market Value represents the price at which a property would normally sell in an open market transaction between a willing buyer and seller.

FMV is commonly used when calculating capital gains tax in situations such as:

• property purchased before 1 April 2001

• inherited property sales

• gifted property sales

• capital gains disputes with tax authorities

To understand FMV rules in detail, see:

[How to Determine Fair Market Value (FMV) of Property as on 1 April 2001]

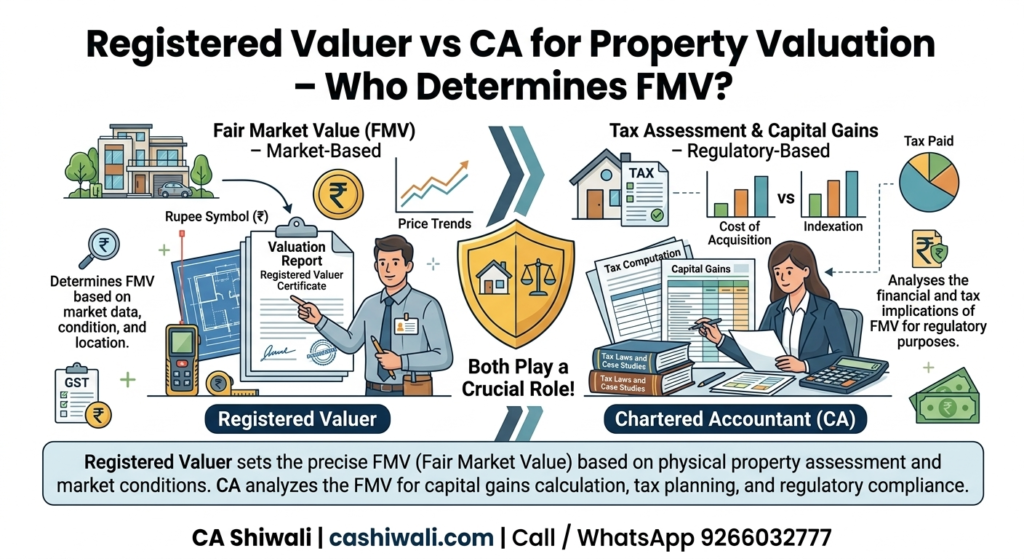

Who is a Registered Valuer?

A registered valuer is a professional who is authorised under valuation regulations to estimate the market value of assets such as land, buildings, and machinery.

Registered valuers prepare formal valuation reports that may be used for:

• property valuation

• bank loan approvals

• income tax proceedings

• dispute resolution

Their reports are often accepted as supporting evidence in tax matters.

Role of a Chartered Accountant in Property Valuation

A Chartered Accountant focuses on tax computation and compliance rather than estimating the physical value of the property.

For capital gains purposes, a CA typically assists with:

• capital gains tax calculation

• applying indexation benefits

• determining taxable gain

• claiming exemptions under tax provisions

A CA also ensures that the valuation used is consistent with the Income Tax Act.

Registered Valuer vs CA – Key Difference

| Aspect | Registered Valuer | Chartered Accountant |

|---|

| Main role | Estimate market value of property | Calculate capital gains tax |

| Type of work | Property valuation report | Tax computation |

| When required | When valuation needs formal support | When calculating tax liability |

| Focus | Market value of asset | Tax planning and compliance |

In many cases, both professionals may be involved in the process.

When a Registered Valuer is Recommended

Obtaining a valuation report may be useful when:

• the property was purchased decades ago

• FMV as on 1 April 2001 needs to be determined

• the property value is very high

• there is a possibility of tax scrutiny

A valuation report can help support the value used for capital gains calculation.

When a Chartered Accountant is Required

A Chartered Accountant is essential when:

• calculating capital gains tax

• applying indexation benefits

• claiming exemptions under Section 54 or Section 54F

• planning reinvestment to reduce tax

The CA ensures the tax computation follows income tax rules.

Do You Need Both Professionals?

In many property sale transactions, both professionals play different roles.

The registered valuer estimates the property value, while the Chartered Accountant calculates the capital gains tax and ensures proper compliance.

This combined approach helps avoid errors in valuation and taxation.