Indexed Cost of Acquisition for Property in India (Complete Guide)

Selling property in India can result in capital gains tax, but the government allows an important benefit called indexation to reduce the taxable amount. Understanding the indexed cost of acquisition for property is essential to calculate the correct long-term capital gains and avoid paying excess tax.

This guide explains what indexed cost of acquisition means, how it is calculated, and how it reduces your capital gains tax liability, with practical examples.

If you need help calculating your capital gains or filing taxes after selling property, you can consult CA Shiwali – Capital Gains Tax Specialist.

Call / WhatsApp CA Shiwali: +91-92660-32777

Call / WhatsApp CA Shiwali: +91-92660-32777

What is Indexed Cost of Acquisition?

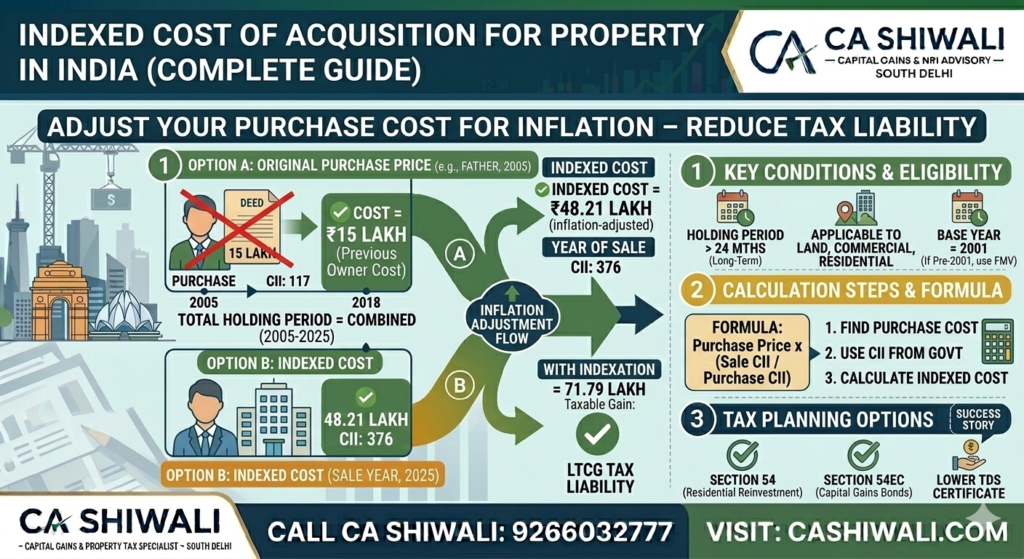

The indexed cost of acquisition adjusts the original purchase price of a property to account for inflation over time.

Since property values increase over the years due to inflation, the Income Tax Act allows taxpayers to increase their purchase cost using the Cost Inflation Index (CII) before calculating capital gains.

This adjustment reduces the taxable gain when the property is sold.

Simply put:

Indexed cost of acquisition = Original purchase price adjusted for inflation.

Cost Inflation Index (CII)

The Cost Inflation Index (CII) is published by the Income Tax Department every year. It measures inflation and is used to calculate the indexed cost of acquisition.

Here are some example values:

| Financial Year | Cost Inflation Index |

|---|---|

| 2001-02 | 100 |

| 2010-11 | 167 |

| 2015-16 | 254 |

| 2020-21 | 301 |

| 2023-24 | 348 |

The base year for indexation is 2001.

If a property was purchased before 2001, the fair market value as of 1 April 2001 can be used as the cost of acquisition.

Indexed Cost of Acquisition Formula

The formula used to calculate indexed cost is:

Indexed Cost of Acquisition = Purchase Price × (CII of Sale Year / CII of Purchase Year)

This formula increases the purchase price based on inflation between the purchase year and the sale year.

Example Calculation

Let’s understand with a simple example.

Property purchase price: ₹20,00,000

Year of purchase: 2005

Year of sale: 2024

CII values:

Purchase year CII = 117

Sale year CII = 348

Indexed cost calculation:

₹20,00,000 × (348 / 117)

Indexed Cost = ₹59,48,717 (approx)

If the property is sold for ₹80,00,000, the capital gain would be calculated as:

Sale price: ₹80,00,000

Indexed cost: ₹59,48,717

Long-term capital gain = ₹20,51,283

Without indexation, the gain would have been ₹60,00,000, so indexation significantly reduces tax liability.

When Indexation Benefit Applies

Indexation benefit is available when the property qualifies as a long-term capital asset.

For real estate in India:

Property held for more than 24 months is considered long-term.

Indexation benefits apply to:

Residential property

Commercial property

Land

When Indexation Does Not Apply

Indexation benefit is not available in the following situations:

Property held for less than 24 months

Certain special tax regimes

In these cases, capital gains are taxed as short-term capital gains, which are usually added to your total income.

Special Cases in Property Capital Gains

Indexation rules can vary depending on how the property was acquired.

Inherited Property

If the property was inherited, the purchase cost and holding period of the previous owner are considered.

Gifted Property

For gifted property, the original purchase price of the previous owner becomes the cost of acquisition.

Property Purchased Before 2001

If the property was purchased before 1 April 2001, the taxpayer can choose:

Original purchase price, or

This rule helps reduce capital gains tax significantly.

In some cases, capital gains may be calculated using stamp duty value under Section 50C rules.

If the property has multiple owners, see our guide on capital gains for jointly owned property.

How CA Shiwali Can Help

Capital gains calculations often become complex due to:

Indexation rules

Cost inflation index selection

Gifted or inherited property cases

Even small mistakes in capital gains calculation can lead to incorrect tax filing or unnecessary tax payment.

CA Shiwali specializes in capital gains tax planning and filing for property transactions in India.

Services include:

Capital gains tax calculation

Indexation calculation

Lower TDS certificate for property sale

Tax planning under Section 54

NRI property sale taxation

Income tax return filing

Call / WhatsApp CA Shiwali: +91-92660-32777

Expert assistance can help ensure accurate tax calculation and maximum legal tax savings.

Conclusion

The indexed cost of acquisition is an important concept in property taxation that helps adjust the purchase price of a property for inflation. By applying the Cost Inflation Index, taxpayers can significantly reduce their capital gains tax liability when selling property.

However, correct calculation is essential, especially for cases involving older properties, inherited assets, or gifted properties.

If you are planning to sell property or calculate capital gains tax, professional guidance can help avoid costly errors.

Read our complete guide on Capital gains on property sale in India

Related Capital Gains Guides

Contact CA Shiwali 92660-32777 today for expert capital gains tax assistance.

Direct Consultation with CA Shiwali Dagar

Expert tax planning and compliance services tailored for NRIs, property owners, and businesses. Get professional clarity on your complex tax matters today.

Strategic Planning

- ✔ Capital Gains (Sec 54/54F)

- ✔ FMV Valuation (Pre-2001)

- ✔ NRI TDS & Form 13

Tax Compliance

- ✔ IT Notice Resolution

- ✔ 15CA & 15CB Certificates

- ✔ GST & Statutory Audits

Start Your Consultation

Whatspp CA Shiwali Now Call CA Shiwali nowProven Results. Online & Offline.