phone

+91-9266032777

email

CaShiwalidagar@gmail.com

🏠 Indexation in Property Sale – How It Reduces Capital Gains Tax (2026 Guide)

🏠 Indexation in Property Sale – How It Reduces Capital Gains Tax (2026 Guide)

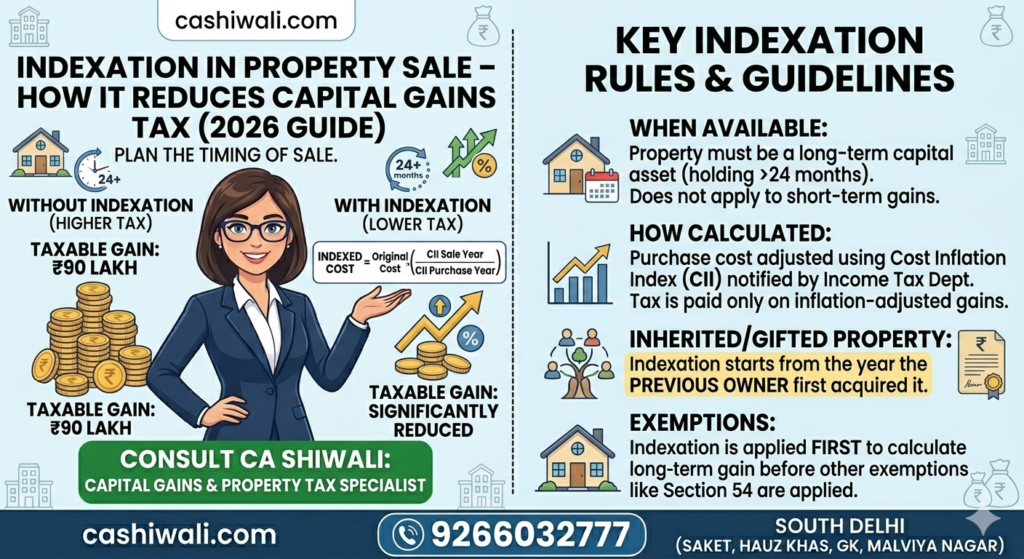

Selling property without understanding indexation can result in paying significantly higher capital gains tax.

Indexation is one of the most powerful legal tools available to reduce long-term capital gains on real estate transactions.

This guide explains how indexation works in property sale and how it reduces your tax liability in 2026.

📍 Capital Gains Advisory – South Delhi

📞 CA Shiwali – 9266032777

What is Indexation in Property Sale?

Indexation adjusts the purchase cost of property for inflation using the Cost Inflation Index (CII) notified by the Income Tax Department.

Instead of paying tax on the full price difference between purchase and sale, you pay tax only on inflation-adjusted gains.

This significantly reduces taxable capital gains.

When is Indexation Available?

Indexation benefit is available when:

Property qualifies as a long-term capital asset

Holding period exceeds prescribed limits (generally more than 24 months for immovable property)

It does not apply to short-term capital gains.

How Indexed Cost is Calculated

Formula:

Indexed Cost of Acquisition =

Original Cost × (CII of Sale Year ÷ CII of Purchase Year)

Example – How Indexation Reduces Tax

Property purchased in 2005 for ₹30 lakh

Sold in 2026 for ₹1.2 crore

Without indexation:

Gain = ₹90 lakh

With indexation:

Indexed cost increases significantly

Taxable gain reduces substantially

The tax saving can run into lakhs depending on holding period.

Indexation in Case of Inherited Property

In inherited property cases:

Indexation benefit starts from the year in which the previous owner first acquired the property.

Not from the year of inheritance.

- builder agreement capital gains

This is often misunderstood and can drastically impact tax liability.

( inherited property page here)

Indexation vs Short-Term Capital Gains

If property is sold before qualifying as long-term:

No indexation benefit

Taxed at slab rates

Higher tax burden

Planning the timing of sale is critical.

Can Indexation Be Used with Section 54 Exemption?

Yes.

Indexation is applied first to calculate long-term capital gain.

After that, Section 54 or 54F exemption may further reduce taxable amount.

( link to Section 54 page here)

Common Mistakes in Indexation

❌ Using wrong Cost Inflation Index year

❌ Ignoring inherited property rules

❌ Confusing stamp duty valuation adjustments

❌ Not planning sale timing

Professional calculation is recommended before filing ITR.

FAQs on Indexation in Property Sale

1. Is indexation mandatory in long-term property sale?

Yes, long-term capital gains on property are computed after applying indexation benefit.

2. Does indexation apply to gifted property?

Yes, cost and holding period of previous owner are considered for indexation.

3. Can indexation eliminate capital gains completely?

In some long-held property cases, indexed cost may significantly reduce taxable gains, but elimination depends on actual figures.

4. Is indexation available for short-term property sale?

No, short-term capital gains do not get indexation benefit.

Capital Gains Advisory in South Delhi

For complete capital gains planning including Section 54, CGAS compliance, Section 50C adjustments and indexation planning, read our detailed Capital Gains & Property Tax Advisory Guide.

( Capital Gains & Property Tax Advisory Guide page)

📞 9266032777

CA Shiwali – Capital Gains & Property Tax Consultant

South Delhi