Cost of Acquisition When Property Purchase Documents Are Missing (2026 Guide)

In many property sale cases in India, especially for old or inherited properties, the original purchase documents are not available. This creates confusion while calculating capital gains tax because the Income Tax Act requires a valid cost of acquisition to determine taxable gains.

If documents are missing, taxpayers can still determine the cost legally using fair market value, valuation reports, or historical records.

Understanding the correct approach helps avoid excess tax liability and disputes with the Income Tax Department.

Why Cost of Acquisition Matters

Capital gains are calculated using the formula:

Capital Gain = Sale Price – Indexed Cost of Acquisition – Expenses

If cost of acquisition is not determined correctly:

Capital gains may be overstated

Tax liability may increase significantly

Notices from the Income Tax Department may arise

This situation commonly occurs when:

Property was purchased many decades ago

Property was inherited

Property was received through gift

Original sale deed is lost

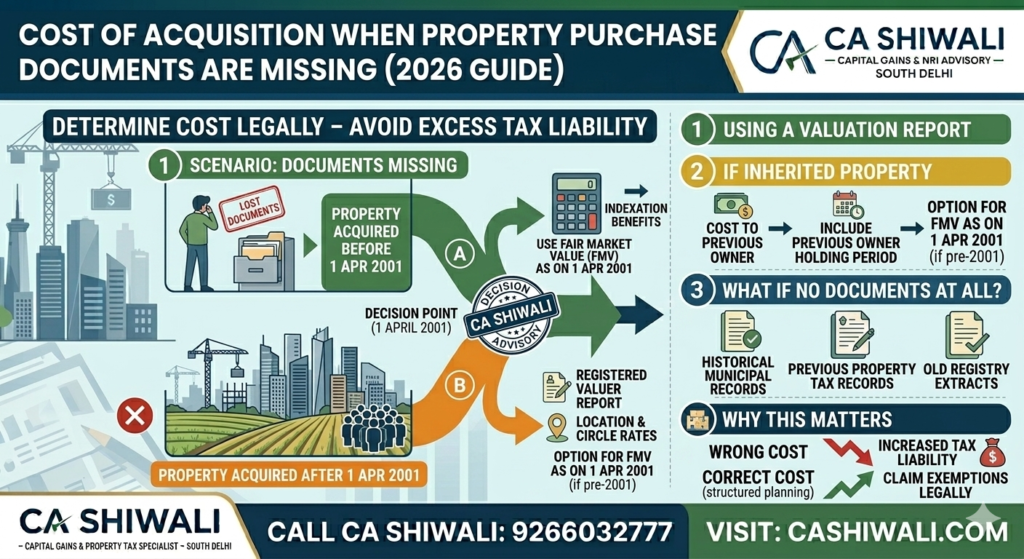

Property Purchased Before 1 April 2001

If the property was purchased before 1 April 2001, the taxpayer can use:

Fair Market Value (FMV) as on 1 April 2001

instead of the original purchase price.

This is permitted under capital gains provisions and helps taxpayers benefit from indexation adjustments.

A registered valuer’s report is often used to determine this value.

Using a Valuation Report

When documents are missing, a registered property valuer may estimate the fair market value of the property.

The valuation report typically considers:

The valuation helps establish a reasonable acquisition cost for tax calculation.

If Property Was Inherited

When property is inherited:

If the previous owner purchased the property before 1 April 2001, the taxpayer may use FMV as of 1 April 2001.

You can read our detailed guide here:

➡ Capital Gains on Inherited Property in India

What If No Documents Exist at All?

If neither purchase documents nor records are available, the following options may be considered:

Valuation report from registered valuer

Historical municipal property records

Previous property tax records

Old property registry extracts

These documents help establish a reasonable basis for determining acquisition cost.

Importance of Proper Documentation

While calculating capital gains, taxpayers should maintain:

Valuation report

Property tax records

Registry extracts

Sale agreement

These documents help justify the cost of acquisition if the Income Tax Department seeks clarification.

Professional Advice Before Selling Property

Determining the correct cost of acquisition is critical before signing a property sale deed.

Proper tax planning can help:

Reduce capital gains tax legally

Claim exemptions under relevant sections

Avoid disputes or tax notices

Planning to sell an old or inherited property?

Proper calculation of capital gains can significantly impact your tax liability.

For professional assistance with capital gains tax planning and property sale taxation, consult:

CA Shiwali – Capital Gains Advisory, South Delhi

📞 Call: 9266032777

FAQ Section

1. What happens if property purchase documents are missing?

If documents are missing, the cost of acquisition may be determined using a valuation report, historical records, or fair market value as permitted under tax rules.

2. Can fair market value be used instead of purchase price?

Yes. For properties acquired before 1 April 2001, the fair market value as of that date may be used.

3. Is valuation report mandatory?

It is not always mandatory but strongly recommended when original documents are unavailable.

4. How is cost calculated for inherited property?

Cost to the previous owner is treated as the cost of acquisition for the current owner.

5. Does indexation apply in such cases?

Yes, indexation benefits apply for long-term capital assets when calculating capital gains.