phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Capital Gains on Gifted Property in India

Capital Gains on Gifted Property in India

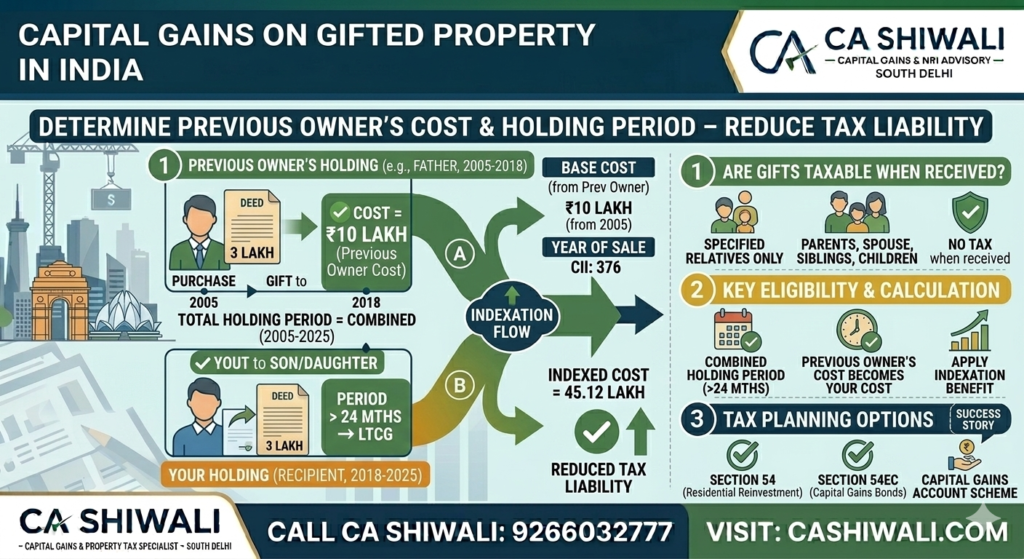

When a property is received as a gift, the tax treatment during sale is different from a normal property purchase. Under the Income Tax Act, the cost of acquisition and holding period of the previous owner are considered when calculating capital gains.

Understanding these rules is important to correctly determine the capital gains tax payable when selling gifted property.

Are Gifts Taxable in India?

Receiving property as a gift is generally not taxable if it is received from specified relatives such as:

Parents

Spouse

Children

Siblings

Grandparents

Lineal ascendants or descendants

However, capital gains tax may apply when the gifted property is sold.

if the property was originally purchased before 2001, the fair market value rule may apply. Learn more in our guide on capital gains on property purchased before 2001.

Cost of Acquisition for Gifted Property

When calculating capital gains, the cost of acquisition is not zero.

Instead, the law states that the cost to the previous owner becomes the cost to the recipient.

Example

| Details | Amount |

|---|---|

| Original purchase price by father | ₹10,00,000 |

| Gifted to son | 2015 |

| Sold by son | ₹80,00,000 |

The cost of acquisition remains:

₹10,00,000

Holding Period for Gifted Property

The holding period includes the period the previous owner held the property.

This means:

Holding Period = Previous Owner Holding + Your Holding

If the combined holding period exceeds 24 months, the gain becomes long-term capital gains (LTCG).

Indexation Benefit for Gifted Property

For long-term capital gains, the taxpayer can apply indexation on the original cost of acquisition.

Formula:

Indexed Cost =

Original Cost × (CII of Sale Year / CII of Purchase Year)

Original Cost × (CII of Sale Year / CII of Purchase Year)

This reduces the taxable capital gains amount.

Example of Capital Gains Calculation

| Details | Amount |

|---|---|

| Father purchased property | 2005 |

| Purchase price | ₹15,00,000 |

| Gifted to daughter | 2018 |

| Sold in | 2025 |

| Sale price | ₹1,20,00,000 |

Step 1: Indexed Cost

Assuming CII:

2005–06 = 117

2025–26 = 376

Indexed Cost =

15,00,000 × (376 / 117)

Indexed Cost ≈ ₹48,20,512

Step 2: Capital Gains

Capital Gains =

1,20,00,000 – 48,20,512

Capital Gains ≈ ₹71,79,488

This amount will be taxed as long-term capital gains at 20% with indexation.

Capital Gains Exemptions Available

Taxpayers selling gifted property can claim the same exemptions as normal property sales.

Section 54

If capital gains are invested in another residential property.

Section 54EC

Investment in capital gains bonds issued by NHAI or REC.

Capital Gains Account Scheme

If a new property is planned but not yet purchased.

These options can significantly reduce the tax liability.

When a property is jointly owned and later gifted, the tax implications may differ. See our guide on capital gains on joint property in India.

Documents Required

When selling gifted property, taxpayers should keep:

Gift deed

Previous owner’s purchase documents

Sale agreement

Improvement expense records

Proof of exemption investments

Proper documentation helps avoid tax disputes.

Professional Help for Gifted Property Capital Gains

Capital gains calculations for gifted property can become complex, especially when determining the previous owner’s cost and holding period.

CA Shiwali assists property owners with:

Capital gains calculation for gifted property

Section 54 and 54EC exemption planning

Capital gains tax filing and compliance

- If you need assistance calculating capital gains or claiming exemptions, you can consult CA Shiwali for capital gains tax planning and compliance.

Professional guidance helps ensure accurate tax calculations and proper documentation.

Frequently Asked Questions

Is gifted property taxable when received?

No, gifts from specified relatives are generally not taxable when received.

Who pays capital gains tax on gifted property?

The person who sells the property is responsible for paying capital gains tax.

What is the cost of acquisition for gifted property?

The previous owner’s purchase price becomes the cost of acquisition.

Can indexation benefit be claimed?

Yes, if the property qualifies as a long-term capital asset, indexation benefit can be applied.

About CA Shiwali

CA Shiwali is a Chartered Accountant specializing in capital gains taxation, property transactions, and real estate tax planning. She advises individuals on tax implications related to inherited, gifted, and jointly owned properties.