phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Capital Gains on Joint Property Sale – Tax Calculation Guide (2026)

Capital Gains on Joint Property Sale – Tax Calculation Guide (2026)

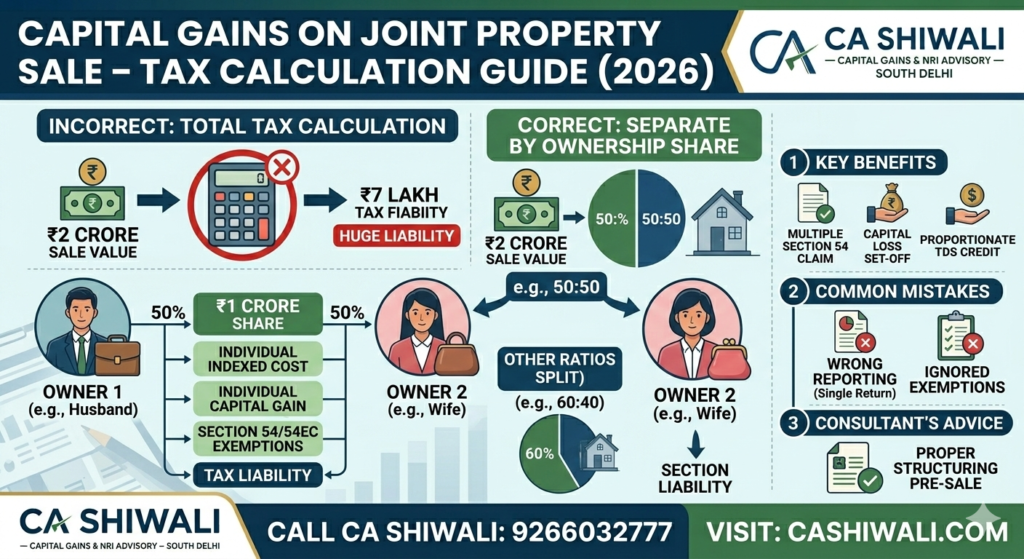

When a jointly owned property is sold, capital gains tax is calculated separately for each co-owner based on their share.

Many taxpayers assume tax is calculated on total sale value jointly. This is incorrect.

Each co-owner is taxed individually.

📍 Property & Capital Gains Consultant – South Delhi

📞 CA Shiwali – 9266032777

How Capital Gains is Calculated in Joint Property

Capital gains are computed separately for each co-owner based on:

Ownership share

Cost of acquisition

Holding period

Individual exemptions

If property is owned 50:50:

Each owner reports 50% of:

Sale consideration

Indexed cost

Capital gain

Example – Joint Sale Calculation

Sale value: ₹2 crore

Ownership: Husband 50%, Wife 50%

Each reports:

₹1 crore sale value

Individual indexed cost

Individual capital gain

Each can claim:

Section 54 exemption

Section 54F exemption

Capital loss set-off

Separately.

What If Ownership Shares Are Different?

If sale deed specifies:

60:40

70:30

Tax will be computed in that ratio.

If no ratio mentioned, it is generally assumed equal unless documented otherwise.

Joint Property With Different Investment Contribution

Important principle:

Capital gains is usually based on legal ownership, not contribution amount.

Unless proper documentation exists, income tax department follows ownership ratio in title deed.

Joint Property – TDS Implications

If property value exceeds ₹50 lakh:

Buyer deducts TDS under Section 194IA (for residents)

Deduction is proportionate to each co-owner

If NRI co-owner is involved:

Higher TDS provisions apply separately

Can Each Co-owner Claim Section 54?

Yes.

If both reinvest in separate residential houses (subject to law conditions), both can claim exemption individually.

This significantly reduces tax liability.

Joint Property Received Through Inheritance

If inherited by multiple heirs:

Each heir’s cost is derived from previous owner

Holding period includes previous owner’s holding

( link to inherited property page)

Common Mistakes in Joint Property Sale

❌ Reporting full capital gains in one person’s return

❌ Incorrect ownership ratio

❌ Ignoring individual exemption eligibility

❌ Wrong TDS credit claim

builder agreement capital gains

Proper structuring before execution of sale deed is recommended.

FAQs – Joint Property Capital Gains

1. Is capital gains divided equally in joint ownership?

It depends on ownership share mentioned in title deed.

2. Can both husband and wife claim Section 54?

Yes, subject to reinvestment conditions.

3. Who receives TDS credit?

Each co-owner receives TDS credit proportionate to their share.

4. What if one co-owner is NRI?

Higher TDS provisions apply separately for that owner.

Joint Property Capital Gains Consultant – South Delhi

If you are planning to sell jointly owned property in South Delhi or Delhi NCR, proper structuring can significantly reduce tax exposure.

📞 9266032777

CA Shiwali – Capital Gains & Property Tax Specialist

Read our complete Capital Gains & Property Advisory Guide for structured planning.