phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Capital Gains Tax on Inherited or Gifted Property in India (2026 Guide)

Capital Gains Tax on Inherited or Gifted Property in India (2026 Guide)

Selling inherited or gifted property can create confusion about capital gains tax calculation.

Many taxpayers are unsure about:

What is the cost of acquisition?

From which year does indexation apply?

What if original purchase documents are missing?

Does Section 54 exemption apply?

This guide explains capital gains rules on inherited and gifted property in India (2026).

📞 Property Tax Advisory – CA Shiwali

📍 South Delhi

📞 9266032777

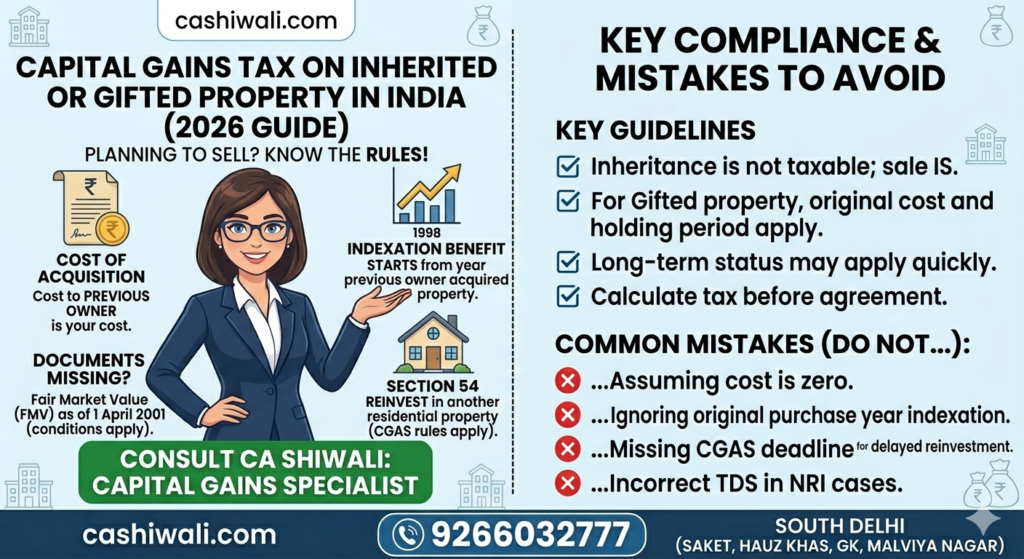

Is Inherited Property Taxable?

Inheritance itself is not taxable in India.

However, when you sell inherited property, capital gains tax becomes applicable.

The key question is:

How is capital gain calculated?

What is the Cost of Acquisition for Inherited Property?

Under Income Tax provisions:

The cost to the previous owner is treated as your cost of acquisition.

This means:

If your father purchased property in 1998 for ₹20 lakh

And you inherited it in 2022

And sold it in 2026

Your cost will be ₹20 lakh (not zero).

From Which Year Does Indexation Apply?

This is where many people make mistakes.

Indexation benefit starts from:

👉 The year in which the previous owner first acquired the property.

Not from the year you inherited it.

This can significantly reduce taxable capital gains.

Example – Capital Gains on Inherited Property

Property purchased by father in 1998 for ₹20 lakh

Inherited in 2022

Sold in 2026 for ₹1.5 crore

Indexed cost calculated from 1998

Taxable gain reduced substantially

Proper indexation can save lakhs.

Capital Gains on Gifted Property

For gifted property:

Cost to original owner becomes your cost

Holding period of original owner is also considered

Long-term classification may apply immediately

This is very important for family gift transactions.

What If Purchase Documents Are Missing?

In old inherited cases:

Fair Market Value (FMV) as of 1 April 2001 may be considered (subject to conditions)

Registered valuer report may be required

Documentation is critical.

Can Section 54 Exemption Be Claimed?

Yes.

If inherited residential property is sold and:

It qualifies as long-term capital asset

Sale proceeds are reinvested in another residential house

Then Section 54 exemption may apply.

CGAS rules may also apply if reinvestment is delayed.

For complete property tax planning in South Delhi, read our detailed Capital Gains & Property Advisory Guide.

Common Mistakes in Inherited Property Sales

❌ Ignoring indexation from original purchase year

❌ Assuming cost is zero

❌ Not checking long-term eligibility

❌ Missing CGAS deposit deadline

❌ Incorrect TDS in NRI cases

Advance planning is strongly recommended.

Who Should Seek Professional Advice?

Individuals selling ancestral property

Family partition cases/ Joint property capital gains

High-value South Delhi property transactions

Property Tax Consultation in South Delhi

If you are planning to sell inherited or gifted property, calculate tax correctly before signing agreement.

📞 9266032777

CA Shiwali – Capital Gains & Property Tax Specialist

South Delhi