phone

+91-9266032777

email

CaShiwalidagar@gmail.com

🏗 Capital Gains on Builder Agreement / Redevelopment – Section 45(5A) Guide (2026)

Capital Gains on Builder Agreement / Redevelopment – Section 45(5A) Guide (2026)

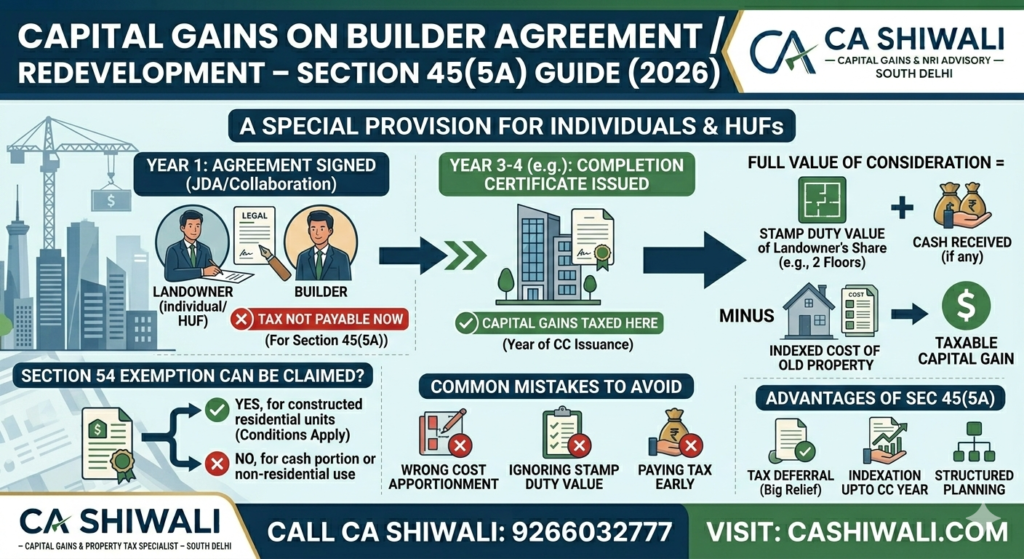

When an individual enters into a builder agreement or redevelopment arrangement, taxation does not happen immediately in the year of signing.

Special provisions under Section 45(5A) apply to individuals and HUFs.

Improper planning can result in unexpected tax liability.

📍 Capital Gains & Property Advisory – South Delhi

📞 CA Shiwali – 9266032777

What is a Builder / Redevelopment Agreement?

In South Delhi, common arrangements include:

Collaboration agreement

Joint development agreement (JDA)

Floor-wise redevelopment

Builder shares constructed floors with landowner/NRI land owner

Instead of full cash consideration, landowner receives:

Constructed area

Sometimes partial cash

When is Capital Gains Taxed? (Section 45(5A))

Under Section 45(5A):

Capital gains are taxable in the year when completion certificate is issued by competent authority — not when agreement is signed.

This is major relief for landowners.

How is Capital Gains Calculated?

Full value of consideration =

Stamp duty value of landowner’s share in project

Cash received (if any)

Then:

Indexed cost of acquisition is deducted

Long-term capital gains taxed at 20%

Example – Redevelopment Case

Landowner gives old house to builder.

Receives:

2 newly constructed floors

₹50 lakh cash

Taxable value = Stamp duty value of 2 floors + ₹50 lakh

Tax payable in year of completion certificate.

What if Builder Delays Completion?

If completion certificate is not issued:

Capital gains is deferred until certificate issuance.

But planning must be structured carefully.

Can Section 54 Be Claimed?

Yes.

If landowner receives residential units, exemption may apply subject to conditions.

TDS Implications in Builder Agreement

Section 194-IC may apply in some cases.

Proper structuring of agreement is critical to avoid unintended tax consequences.

Common Mistakes in Redevelopment Taxation

❌ Paying tax in year of agreement

❌ Ignoring stamp duty valuation

❌ Incorrect cost apportionment

❌ Not planning exemption in advance

❌ Not documenting constructed area value

These cases require professional review before signing builder agreement.

FAQs – Builder Agreement Capital Gains

1. When is capital gains taxable in redevelopment?

In the year when completion certificate is issued under Section 45(5A).

2. Is tax payable when agreement is signed?

Generally no, if Section 45(5A) conditions are satisfied.

3. How is sale value determined?

Based on stamp duty value of landowner’s share plus any cash received.

4. Can Section 54 exemption be claimed?

Yes, subject to reinvestment and residential property conditions.

Builder Agreement Tax Consultant – South Delhi

If you are planning redevelopment or collaboration agreement in South Delhi or Delhi NCR, tax planning before signing agreement can significantly reduce risk.

📞 9266032777

CA Shiwali – Capital Gains & Property Tax Specialist

Read our complete Capital Gains & Property Advisory Guide for structured planning.