- Our Services

- Capital Gains Tax (Save Tax on Property Sale)

- Save Capital Gains Tax (Section 54 / 54F)

- Section 50C (Stamp Duty Rule)

- CGAS Scheme

- Fair Market Value (FMV) for Capital Gains 2001

- Joint Property Sale Tax

- NRI Taxation (Property & ITR)

- TDS on NRI Property

- NRI Avoid DTAA/ ITR Filing

- Repatriation

- NRI Property Sale Tax

- Income Tax Notice Help ⚡

- Scrutiny Cases

- Income Tax Notice Reply

- GST Notices

- Tax Notice 143

- Calculate Capital Gains Tax (Free Tool)

- Company / LLP Registration

- GST Registration & Filing

- ITR Filing Services

- About CA Shiwali

- Tax Blog/ Guide

- Contact

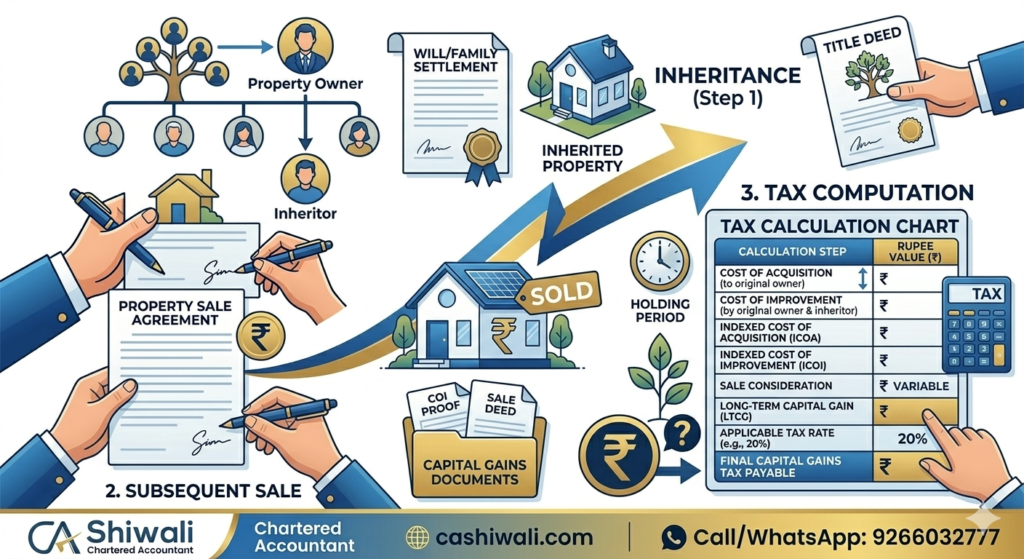

Capital Gains on Inherited Property Calculator (India)

When a person sells inherited property, capital gains tax may apply depending on the holding period and the difference between the sale price and the indexed cost of acquisition.

Under Indian tax law, inherited property is taxed based on the original cost to the previous owner and the holding period includes the period for which the previous owner held the asset.

Our calculator helps estimate the potential capital gains when selling inherited property.

Inherited Property Tax Advisor

FY 2026-27 Advanced Edition

Indexed Cost of Acquisition:

-

Option A (12.5%)

-

Option B (20% Indx)

-

Capital Gains Tax on Inherited Property in India – Complete Guide

Selling inherited property can lead to capital gains tax, but the calculation rules are slightly different from normal property sales. Many taxpayers mistakenly assume that capital gains will be calculated based on the value of the property at the time of inheritance. However, the Income Tax Act provides specific provisions that determine how the cost of acquisition should be calculated in such cases.

Under Section 49 of the Income Tax Act, when a taxpayer receives property through inheritance, gift, or succession, the cost of acquisition is considered to be the cost paid by the previous owner. This means that the original purchase price paid by the person from whom the property was inherited becomes the base for capital gains calculation.

In addition to the cost rule, the holding period of the previous owner is also counted while determining whether the asset is long-term or short-term. Because inherited properties are often held by the previous owner for many years, they are usually treated as long-term capital assets when sold.

Our Capital Gains on Inherited Property Calculator helps estimate the indexed cost and potential capital gain when selling inherited property.

How Capital Gains on Inherited Property is Calculated

The capital gains calculation involves three main components:

1. Sale Price of Property

This is the value at which the inherited property is sold.

However, if the property is sold at a value lower than the stamp duty value determined by the registrar, the provisions of Section 50C of the Income Tax Act may apply. In such cases, the stamp duty value may be considered as the sale value for tax calculation.

2. Cost of Acquisition

The cost of acquisition is the original purchase price paid by the previous owner, not the value at which the property was inherited.

For example:

If your father purchased a property in 1995 for ₹5,00,000 and you inherited it in 2015, the cost of acquisition will still be ₹5,00,000 for tax calculation.

3. Indexation Benefit

When inherited property is treated as a long-term capital asset, taxpayers can claim indexation benefit, which adjusts the cost of acquisition based on inflation.

The indexed cost is calculated using the Cost Inflation Index (CII) published by the government.

Indexed Cost = Original Cost × (CII of Sale Year ÷ CII of Purchase Year)

This significantly reduces the taxable capital gain.

You can estimate this easily using our Capital Gains Indexation Calculator available on this website.

Example of Capital Gains on Inherited Property

Consider the following example:

Original purchase price (father bought property in 2000): ₹10,00,000

Sale price in 2025: ₹90,00,000

CII for 2000: 100

CII for 2025: 348

Indexed cost =

10,00,000 × (348 / 100)

Indexed cost = ₹34,80,000

Capital gain =

₹90,00,000 − ₹34,80,000

Capital gain = ₹55,20,000

The taxpayer will pay long-term capital gains tax on this amount unless exemptions are claimed.

Tax Saving Options for Inherited Property Sale

The Income Tax Act provides several exemptions that can help reduce capital gains tax.

Section 54 – Investment in Residential Property

If the inherited property sold is a residential house, the taxpayer may claim exemption under Section 54 of the Income Tax Act by investing the capital gain in another residential property.

Section 54 Capital Gains Exemption

If you are reinvesting the capital gains from a property sale into another residential property, you may claim exemption under Section 54 of the Income Tax Act.

See our complete guide on Section 54 & Section 54F capital gains exemption on property sale to understand eligibility conditions and tax planning strategies.

You can estimate the eligible exemption using our Section 54 Exemption Calculator.

Section 54F – Investment in House After Selling Other Assets

If the inherited property sold is land or another asset and the proceeds are invested in a new residential house, exemption may be available under Section 54F of the Income Tax Act.

You can check eligibility using our Section 54F Exemption Calculator.

Capital Gains Account Scheme

If you cannot invest the capital gains immediately, the amount can be temporarily deposited under the Capital Gains Account Scheme until it is utilized for purchasing or constructing a new property.

Related Capital Gains Tools on Our Website

To help taxpayers plan property transactions more effectively, you may also use the following calculators:

These tools provide a quick estimate of potential tax liability and help taxpayers understand available exemptions.

Common Mistakes When Selling Inherited Property

Many taxpayers make errors when calculating capital gains on inherited property. Some common mistakes include:

• Using the property value at the time of inheritance instead of the original purchase price

• Ignoring indexation benefits

• Forgetting the impact of stamp duty valuation rules

• Missing available capital gains exemptions

Proper tax planning before selling inherited property can help reduce tax liability significantly.

Frequently Asked Questions (FAQs)

Is inherited property taxable in India?

Inheritance itself is not taxable in India. However, if the inherited property is sold later, capital gains tax may apply based on the difference between the sale price and the indexed cost of acquisition.

What is the cost of acquisition for inherited property?

Under Section 49 of the Income Tax Act, the cost of acquisition is deemed to be the cost paid by the previous owner who originally purchased the property.

Is indexation available for inherited property?

Yes. If the inherited property is treated as a long-term capital asset, the taxpayer can claim indexation benefit to adjust the cost for inflation.

Does stamp duty value affect inherited property sale?

Yes. If the property is sold at a value lower than the stamp duty valuation, Section 50C may apply and the stamp duty value may be considered as the sale price for tax calculation.

How can a capital gains calculator help?

A capital gains calculator helps estimate:

• Indexed cost of acquisition

• Capital gain amount

• Potential tax liability

This allows taxpayers to plan property sales and investments more efficiently.

Need Help With Capital Gains Tax?

Capital gains taxation on inherited property can involve multiple rules, including indexation, exemption provisions, and stamp duty valuation. Professional guidance can help ensure that taxpayers comply with the law while minimizing tax liability.

If you need assistance with capital gains tax planning, property sale taxation, or exemption claims, professional advice can be very helpful.

CA Shiwali

Chartered Accountant – Capital Gains & Property Tax Advisory

🌐 Website: cashiwali.com

📞 Call / WhatsApp: 9266032777

Consultation can help ensure accurate tax calculation and proper planning before selling inherited property.

📌 Related Guides

Posted on GoogleTrustindex verifies that the original source of the review is Google. ⭐⭐⭐⭐⭐ I am extremely grateful to CA Shiwali Dagar for preparing my CA report on very short notice. Despite the urgent timeline, she handled everything professionally, accurately, and efficiently. She was responsive throughout the process, explained the requirements clearly, and delivered the report on time without compromising on quality. Her dedication, attention to detail, and commitment to client satisfaction were truly impressive. I highly recommend CA Shiwali Dagar to anyone looking for reliable and professional Chartered Accountant services, especially when working under tight deadlines.Posted on GoogleTrustindex verifies that the original source of the review is Google. All queries were nicely n professionally handled :)Posted on GoogleTrustindex verifies that the original source of the review is Google. Shiwali was really helpful in getting our 12A ad 80G. Will definitely recommend her services. It was a pleasure working with her.Posted on GoogleTrustindex verifies that the original source of the review is Google. Great service 👍 CA Shiwali is highly professional and detail-oriented. She helped me with my tax filing and guided me properly.Posted on GoogleTrustindex verifies that the original source of the review is Google. She is polite and helpful CAPosted on GoogleTrustindex verifies that the original source of the review is Google. Hi Shiwali, Thank you for your excellent support and guidance. I truly appreciate your professionalism and timely assistance."Posted on GoogleTrustindex verifies that the original source of the review is Google. Thank you Shiwali Mam for your excellent support and guidance throughout my tax filing process. I appreciate your professionalism, prompt responses, and clear explanations of complex tax matters. Your expertise made the entire process smooth and look forward to working with you in the future.Posted on GoogleTrustindex verifies that the original source of the review is Google. I had a great experience with M/s Shiwali & Co. They are highly professional, knowledgeable, and extremely responsive throughout the entire process. From ITR filing to handling income tax-related queries, everything was managed smoothly and efficiently. Their guidance made the entire process completely hassle-free, and they kept me informed with timely updates at every stage. What I appreciated most was their transparency, professionalism, and commitment to delivering results without unnecessary delays. If anyone is looking for reliable support with Income Tax services, I would highly recommend M/s Shiwali & Co. They are a trustworthy, efficient, and dependable consultancy firm.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Expert Financial Advisory

Expert Tax Planning for Your Property Sale

Secure your gains. Minimize your liability with professional intervention from CA Shiwali & Co.

★ Verified Accuracy

Precise indexation & capital gains math.

🛡️ Notice Protection

Professional handling of IT Department inquiries.

🌍 NRI Specialist

TDS & compliance for international sellers.

Ready to file correctly? Connect now:

Direct Consultation with CA Shiwali Dagar

Expert tax planning and compliance services tailored for NRIs, property owners, and businesses. Get professional clarity on your complex tax matters today.

Strategic Planning

- ✔ Capital Gains (Sec 54/54F)

- ✔ FMV Valuation (Pre-2001)

- ✔ NRI TDS & Form 13

Tax Compliance

- ✔ IT Notice Resolution

- ✔ 15CA & 15CB Certificates

- ✔ GST & Statutory Audits

Start Your Consultation

Whatspp CA Shiwali Now Call CA Shiwali nowProven Results. Online & Offline.