Do I Pay Tax If I Sell Property Within 2 Years? (2026 Guide for Property Owners)

Do I Pay Tax If I Sell Property Within 2 Years? (2026 Guide for Property Owners)

Selling a property within 2 years of purchase can have serious tax implications under Indian Income Tax laws.

Many property owners in Delhi assume that profit = capital gains = standard tax.

But the reality is more nuanced.

If you sell property within 24 months, the tax treatment changes completely.

Let’s break it down clearly.

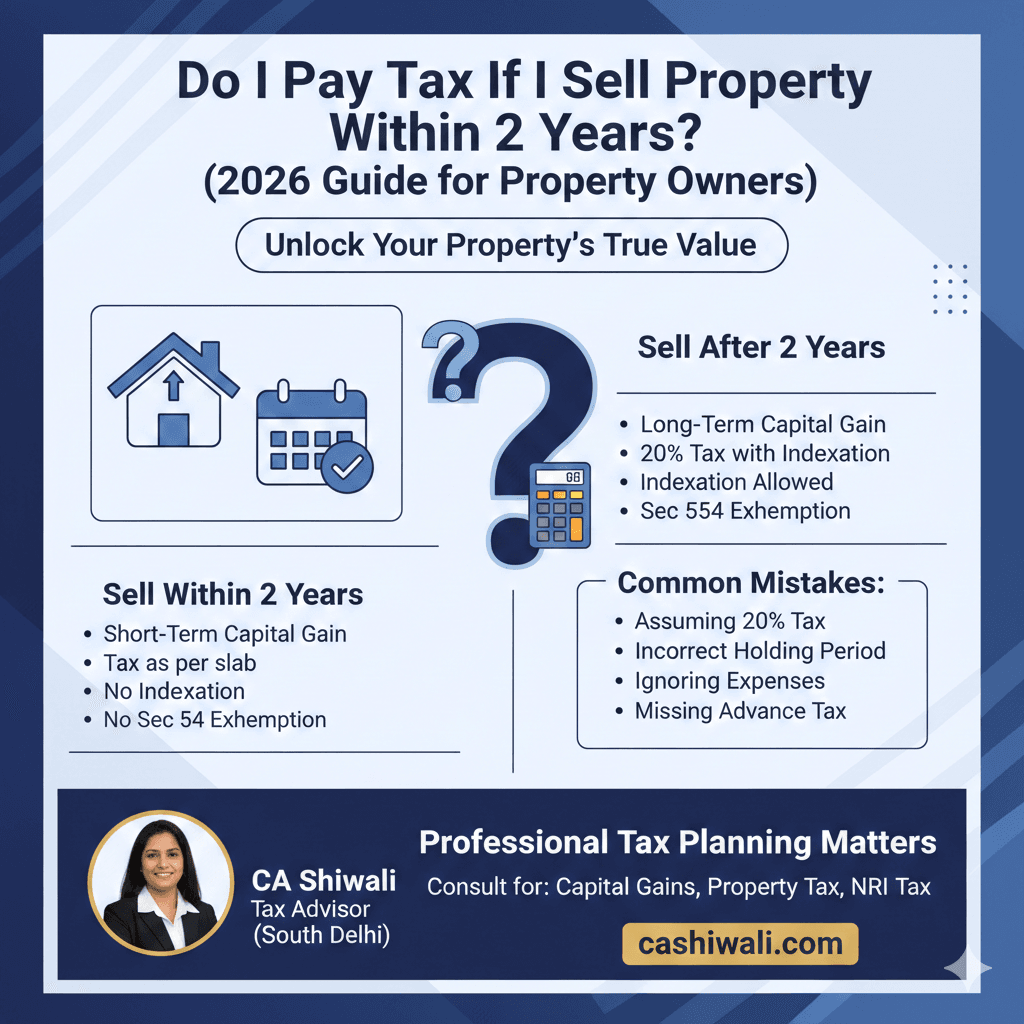

📌 1. What Happens If You Sell Property Within 2 Years?

If you sell an immovable property (house, flat, land) within 24 months of purchase, it is classified as:

Short-Term Capital Gain (STCG)

This is different from Long-Term Capital Gain (LTCG).

📌 2. How Is Short-Term Capital Gain Taxed?

If sold within 2 years:

The profit is added to your total income

Taxed as per your income tax slab

No indexation benefit

No special 20% rate

Example:

If:

Purchase price = ₹50 lakh

Sale price = ₹60 lakh

Gain = ₹10 lakh

This ₹10 lakh will be added to your total income.

If you fall under 30% slab →

Tax = ₹3 lakh + cess.

📌 3. Difference Between STCG and LTCG on Property

| Particular | Sold Within 2 Years | Sold After 2 Years |

|---|---|---|

| Type | Short-Term Capital Gain | Long-Term Capital Gain |

| Tax Rate | As per slab | 20% with indexation |

| Indexation | Not allowed | Allowed |

| Section 54 Exemption | Not available* | Available |

*Section 54 exemption is generally available only for LTCG on residential property.

📌 4. Can You Save Tax If Sold Within 2 Years?

This is where planning matters.

In most cases:

❌ You cannot claim Section 54 exemption

❌ You cannot use indexation

❌ Gain will be taxed as regular income

However, in certain structured scenarios (depending on property type and reinvestment pattern), tax planning may reduce liability.

This requires case-specific evaluation.

📌 5. What If Property Was Booked From Builder?

Important distinction:

The 2-year period is calculated from:

Date of acquisition (usually possession or allotment date depending on case law).

This area is often misunderstood.

Improper calculation can lead to incorrect tax filing.

📌 6. What About TDS on Property Sale?

If property value exceeds ₹50 lakh:

Buyer must deduct 1% TDS under Section 194IA.

If seller is NRI:

TDS can be 20% or more under Section 195.

This is separate from capital gains tax.

📌 7. Common Mistakes People Make

Assuming profit is automatically 20% tax

Ignoring stamp duty value implications

Not adjusting brokerage & transfer expenses

Incorrect holding period calculation

Missing advance tax payment

These mistakes often lead to Income Tax Notices later.

📌 8. Should You Delay Sale Beyond 2 Years?

In many cases, waiting until crossing 24 months can significantly reduce tax burden because:

You shift from slab rate to 20%

You get indexation

You may claim Section 54 exemption

However, market conditions + liquidity needs must also be considered.

📌 9. Professional Tax Planning Matters

Every property sale should be evaluated before execution.

Even a 1-month timing difference can change tax liability by lakhs.

If you are planning to sell property in South Delhi or anywhere in India and want proper capital gains calculation and tax planning, consult a professional before finalizing the deal.

About the Author

CA Shiwali is a practicing Chartered Accountant in South Delhi specializing in Capital Gains Tax, Property Taxation, and NRI Tax advisory.

For consultation regarding property sale taxation, capital gains calculation, or income tax planning, professional guidance is available.

Frequently Asked Questions (FAQs)

1️⃣ Is it compulsory to pay tax if I sell property within 2 years?

Yes. If you sell property within 24 months of purchase, the profit is treated as Short-Term Capital Gain (STCG) and taxed as per your income tax slab rate. There is no flat 20% rate benefit.

2️⃣ How is the 2-year holding period calculated?

The 24-month period is generally calculated from the date of acquisition.

In builder cases, this may depend on allotment date vs possession date, based on legal interpretation. Proper evaluation is important to avoid incorrect tax treatment.

3️⃣ Can I claim Section 54 exemption if I sell within 2 years?

No. Section 54 exemption is generally available only for Long-Term Capital Gains (LTCG) on sale of residential property. If sold within 2 years, exemption benefits are usually not available.

4️⃣ What tax rate applies if I am in the 30% slab?

If you fall under the 30% income tax slab and sell within 2 years, your short-term capital gain will be taxed at 30% (plus cess and surcharge, if applicable).

5️⃣ Can I reduce short-term capital gains tax legally?

Short-term capital gains are taxed as regular income, so deductions are limited. However, strategic tax planning before sale may help optimize your overall tax liability.

6️⃣ What happens if I don’t pay tax on property sale?

If tax is not properly declared:

You may receive an Income Tax notice

Interest under Section 234B and 234C may apply

Penalties may be imposed in certain cases

Timely reporting and advance tax compliance is essential.

7️⃣ Is TDS deducted even if I make no profit?

Yes. If property value exceeds ₹50 lakh, the buyer must deduct 1% TDS under Section 194IA, irrespective of whether you made profit or not.

For NRI sellers, higher TDS under Section 195 may apply.

8️⃣ Should I wait to complete 2 years before selling?

In many cases, waiting beyond 24 months converts STCG into LTCG, which:

Allows indexation benefit

Applies 20% tax rate

Makes Section 54 exemption available

However, decision should consider market conditions and liquidity needs.

Need Professional Help With Capital Gains Calculation?

If you are planning to sell property in South Delhi or anywhere in India and want accurate capital gains calculation, tax planning, or NRI property tax advisory, professional guidance can help you avoid costly mistakes.

CA Shiwali specializes in property taxation and capital gains advisory for individuals and NRIs.

Direct Consultation with CA Shiwali Dagar

Expert tax planning and compliance services tailored for NRIs, property owners, and businesses. Get professional clarity on your complex tax matters today.

Strategic Planning

- ✔ Capital Gains (Sec 54/54F)

- ✔ FMV Valuation (Pre-2001)

- ✔ NRI TDS & Form 13

Tax Compliance

- ✔ IT Notice Resolution

- ✔ 15CA & 15CB Certificates

- ✔ GST & Statutory Audits

Start Your Consultation

Whatspp CA Shiwali Now Call CA Shiwali nowProven Results. Online & Offline.