phone

+91-9266032777

email

CaShiwalidagar@gmail.com

📝 How to Pay Zero Tax in India Legally (2026 Guide)

By CA Shiwali – Cashiwali.com

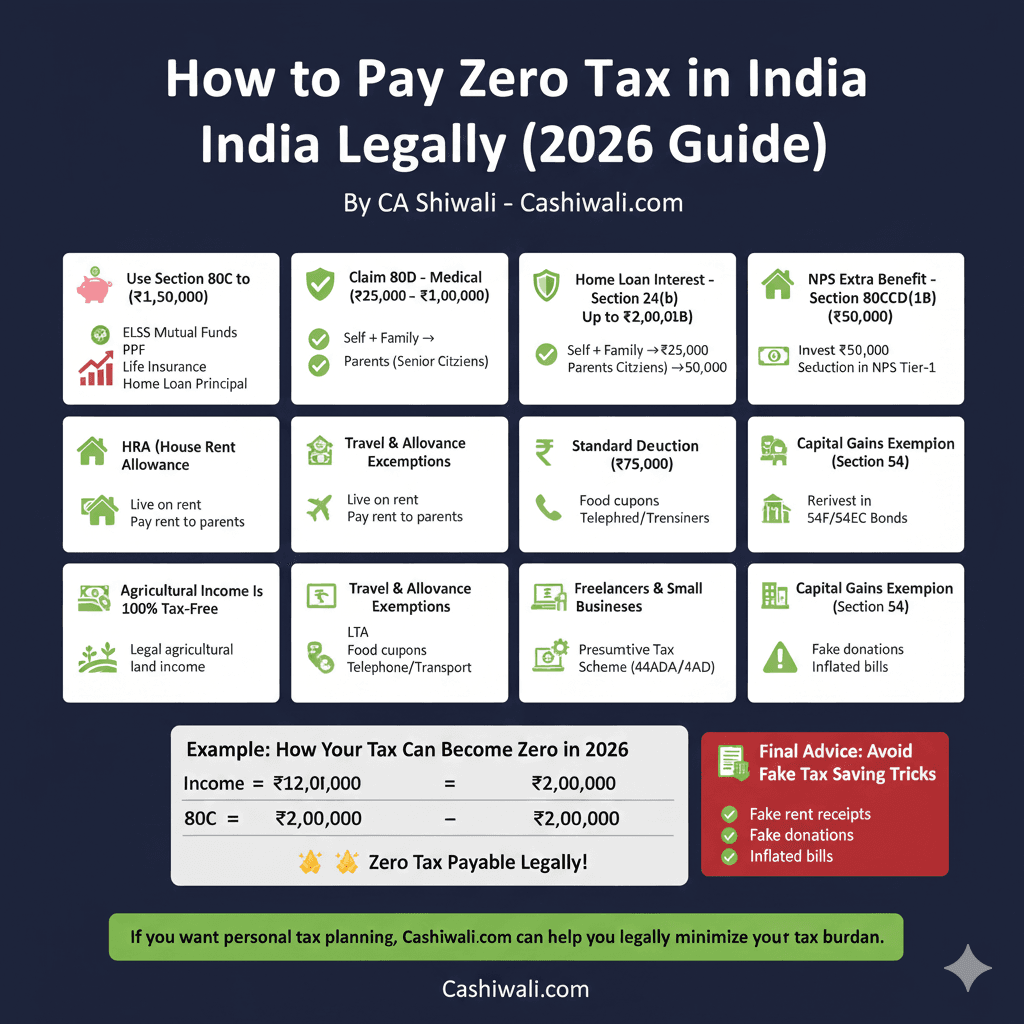

Paying zero tax legally in India is absolutely possible—if you understand the Income Tax Act, exemptions, deductions, new rules, and tax-saving investment opportunities. In 2026, with rising income levels, smart tax planning has become essential for salaried individuals, freelancers, small business owners, and even senior citizens.

This article explains legal, safe, and practical ways to reduce your tax liability to zero, without any loopholes, risk, or penalties.

✅ 1. Use Section 80C to Its Full Limit (₹1,50,000)

Section 80C alone can wipe out a major part of your taxable income.

Popular 80C Options:

ELSS Mutual Funds

PPF (Public Provident Fund)

Life Insurance Premium

NSC (National Savings Certificate)

Home Loan Principal

School Tuition Fee

Maximize this ₹1.5 lakh deduction first.

✅ 2. Claim 80D – Medical Insurance (₹25,000 – ₹1,00,000)

Health insurance gives tax benefits plus medical protection.

For yourself + family → ₹25,000

For parents (senior citizens) → ₹50,000

Total possible → ₹75,000 – ₹1,00,000

✅ 3. Home Loan Interest – Section 24(b) (Up to ₹2,00,000)

If you have a home loan on a self-occupied property, you can claim:

👉 ₹2 lakh deduction on interest

Combined with 80C (principal), this is one of the biggest tax-saving tools.

✅ 4. NPS Extra Benefit – Section 80CCD(1B) (₹50,000)

This is over and above 80C.

If you invest ₹50,000 in NPS Tier-1, you directly reduce taxable income by ₹50,000.

✅ 5. HRA (House Rent Allowance) – Big Tax Saver for Salaried People

If you live on rent, HRA can reduce tax significantly.

You can legally claim HRA even if:

You live in another city for work

You pay rent to parents (with proper documentation)

✅ 6. Travel & Allowance Exemptions (2026 Rules)

Employees get tax-free exemptions like:

LTA (Leave Travel Allowance)

Food coupons

Telephone reimbursement

Transport allowance

Uniform allowance

Most salaried people don’t use these effectively.

✅ 7. Standard Deduction (₹75,000)

From FY 2025-26 onwards, the standard deduction is ₹75,000 for salaried individuals and pensioners.

This alone reduces tax liability drastically.

✅ 8. Capital Gains Exemption through Section 54

If you sell property and reinvest the gains into another residential property, you pay zero tax on capital gains.

Also available:

Section 54F

Section 54EC (NHAI/REC Bonds)

✅ 9. Agricultural Income Is 100% Tax-Free

If you have legal agricultural land and income, it is fully exempt.

But rules of clubbing and proper documentation apply.

✅ 10. Freelancers & Small Businesses – Use Presumptive Tax Scheme

Under Section 44ADA / 44AD, you can report income at a lower taxable percentage.

In many cases, your final tax becomes zero after deductions.

🟩 Example: How Your Tax Can Become Zero in 2026

Let’s say your yearly income = ₹12,00,000

Now reduce:

Standard deduction = ₹75,000

80C = ₹1,50,000

80D = ₹25,000

80CCD(1B) = ₹50,000

Home loan interest = ₹2,00,000

HRA exemption = ₹1,50,000

Your taxable income becomes ₹5,50,000, of which most is covered under Section 87A rebate →

🎉 Zero Tax Payable Legally!

⭐ Final Advice: Avoid Fake Tax Saving Tricks

Don’t use shortcuts like:

✘ Fake rent receipts

✘ Fake donations

✘ Inflated medical bills

✘ Fake business expenses

These can lead to penalties and notices.

If you want personal tax planning, www.Cashiwali.com can help you legally minimize your tax burden.

Direct Consultation with CA Shiwali Dagar

Expert tax planning and compliance services tailored for NRIs, property owners, and businesses. Get professional clarity on your complex tax matters today.

Strategic Planning

- ✔ Capital Gains (Sec 54/54F)

- ✔ FMV Valuation (Pre-2001)

- ✔ NRI TDS & Form 13

Tax Compliance

- ✔ IT Notice Resolution

- ✔ 15CA & 15CB Certificates

- ✔ GST & Statutory Audits

Start Your Consultation

Whatspp CA Shiwali Now Call CA Shiwali nowProven Results. Online & Offline.