phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Lower TDS Certificate for NRI Property Sale in India (Section 197 Guide – 2026)

Lower TDS Certificate for NRI Property Sale in India (Section 197 Guide – 2026)

When a Non-Resident Indian (NRI) sells property in India, buyers are legally required to deduct TDS at higher rates, often resulting in excess tax deduction even when the actual capital gains tax is much lower.

A Lower TDS Certificate under Section 197 allows NRIs to reduce or avoid unnecessary tax deduction and improve cash flow during property transactions.

CA Shiwali assists NRIs in obtaining Lower TDS certificates and ensuring compliant property sale transactions across India.

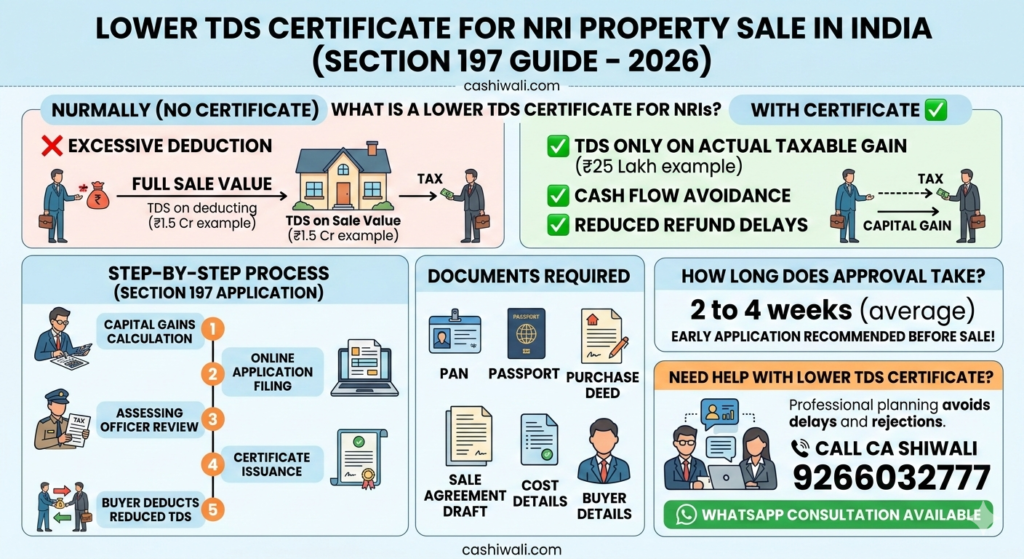

What is a Lower TDS Certificate for NRIs?

A Lower TDS Certificate is issued by the Income Tax Department permitting the buyer to deduct tax at a reduced rate instead of the standard NRI TDS rate.

Normally:

Buyer deducts TDS on full sale value

Not on actual capital gains

This leads to excessive deduction.

With a Lower TDS Certificate:

✅ TDS is deducted only on estimated tax liability

✅ Cash blockage is avoided

✅ Refund delays are reduced

Why NRIs Need a Lower TDS Certificate

Under Indian tax law:

Buyers must deduct TDS under Section 195

Deduction may range between 20%–30%+ surcharge & cess

Applied on entire sale consideration

However, actual capital gains tax may be far lower due to:

Indexation benefit

Exemptions under Section 54 / 54EC

Purchase cost adjustments

Improvement expenses

Without planning, NRIs often lose access to large funds until refund processing.

Example: Excess TDS Without Certificate

Sale Value: ₹1.5 Crore

Actual Capital Gain: ₹25 Lakhs

Without certificate:

TDS deducted on ₹1.5 Cr → huge deduction

With Lower TDS Certificate:

TDS calculated on actual taxable gain

Result:

✔ Immediate liquidity

✔ No long refund wait

Who Can Apply for Lower TDS Certificate?

NRIs selling:

Residential property

Commercial property

Inherited property

Jointly owned property

Eligibility generally applies when:

Capital gain is lower than sale value

Exemption is planned

Loss or minimal gain exists

Documents Required for Lower TDS Application

Typical documents include:

PAN of NRI seller

Passport copy

Property purchase documents

Sale agreement draft

Cost and improvement details

Capital gains computation

Buyer details

Tax residency information

Proper documentation significantly speeds approval.

Step-by-Step Process (Section 197 Application)

Step 1: Capital Gains Calculation

A Chartered Accountant calculates estimated tax liability.

Step 2: Online Application Filing

Application submitted through Income Tax portal under Section 197.

Step 3: Assessing Officer Review

Tax officer reviews documents and calculations.

Step 4: Certificate Issuance

Lower or NIL deduction certificate issued.

Step 5: Buyer Deducts Reduced TDS

Buyer follows certificate rate legally.

How Long Does Approval Take?

Typical timeline:

2 to 4 weeks (average)

May vary depending on jurisdiction and documentation accuracy.

Early application is strongly recommended before executing sale.

Common Mistakes NRIs Make

Many property sellers face issues because:

Application filed after receiving payment

Incorrect capital gain calculations

Missing documents

Buyer already deducted full TDS

Exemption planning done too late

Professional guidance avoids delays and rejection.

Benefits of Applying Before Property Sale

✔ Prevents excess tax deduction

✔ Improves fund availability

✔ Reduces refund dependency

✔ Ensures smooth bank compliance

✔ Avoids disputes with buyer

When Should You Contact a CA?

You should apply for a Lower TDS Certificate if:

Property value exceeds ₹50 lakh

Capital gains are expected to be low

Exemption under Section 54/54EC planned

Property held for long duration

You need funds repatriated abroad

Planning should begin before signing the final sale deed.

How CA Shiwali Assists NRIs

Services include:

Capital gains computation

Section 197 application filing

Documentation review

Coordination with tax authorities

TDS compliance guidance

Post-sale tax filing support

Professional handling ensures compliance while optimising tax deduction legally.

Frequently Asked Questions (FAQs)

Is Lower TDS Certificate mandatory for NRIs?

No, but it helps avoid excess deduction and refund delays.

Can TDS be reduced to zero?

Yes, if taxable capital gain is negligible or exemptions fully apply.

Who applies — buyer or seller?

The NRI seller applies through a Chartered Accountant.

What if buyer already deducted full TDS?

Refund can still be claimed through income tax return filing.

Is the certificate valid for all buyers?

It applies only to the specific transaction mentioned.

Need Help With Lower TDS Certificate for NRI Property Sale?

Incorrect TDS deduction can block substantial funds for months.

Professional planning ensures smoother transactions and accurate compliance.

📞 Call CA Shiwali

💬 WhatsApp 9266032777 Consultation Available