phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Capital Gains Tax on Property for NRIs in India (2026)

Capital Gains Tax on Property for NRIs in India (2026)

Non-Resident Indians (NRIs) selling property in India are subject to capital gains tax, just like resident Indians. However, the tax rates, TDS rules, exemptions, and compliance requirements for NRIs are different and often misunderstood.

This page explains capital gains tax on property for NRIs in simple terms — when it applies, how it is calculated, and how NRIs can legally reduce or plan their tax liability in India.

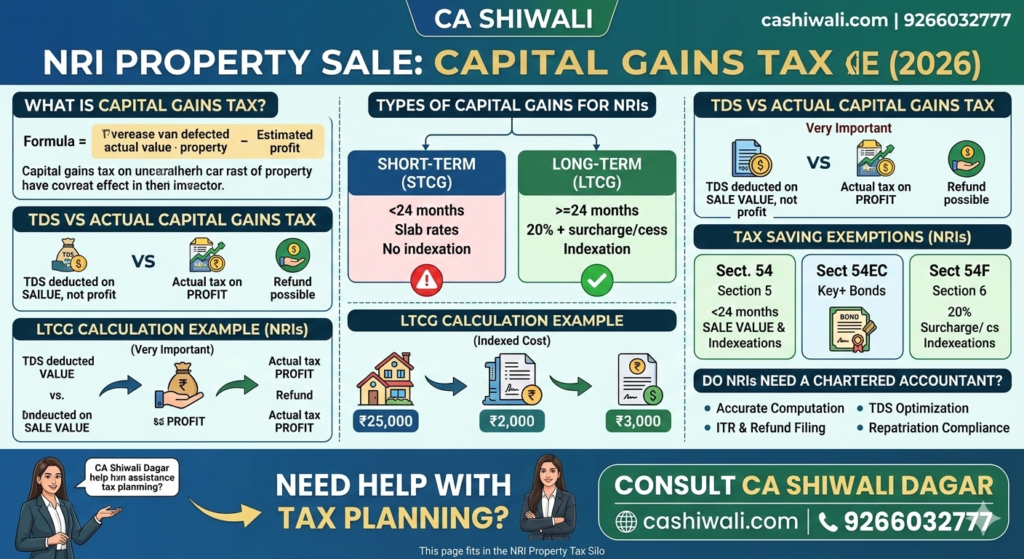

What Is Capital Gains Tax on Property?

Capital gains tax is the tax payable on the profit earned from selling a property.

Capital Gain = Sale Price – (Purchase Cost + Allowed Expenses)

For NRIs, capital gains tax applies whether:

The sale proceeds remain in India, or

The money is repatriated abroad

Types of Capital Gains for NRIs

Capital gains are classified based on the holding period of the property.

Short-Term Capital Gains (STCG)

Holding period: Less than 24 months

Tax rate: As per applicable income tax slab

Indexation benefit: ❌ Not allowed

📌 Short-term capital gains are fully taxable and usually result in higher tax liability.

Long-Term Capital Gains (LTCG)

Holding period: 24 months or more

Tax rate: 20% + surcharge + cess

Indexation benefit: ✅ Allowed

📌 Most NRI property transactions fall under long-term capital gains.

How Is Capital Gains Calculated for NRIs?

For Long-Term Capital Gains:

Purchase price is adjusted using Cost Inflation Index (CII)

This reduces the taxable gain legally

Example (simplified):

Purchase price (indexed): ₹50 lakh

Sale price: ₹80 lakh

Long-term capital gain: ₹30 lakh

Tax @20% = ₹6 lakh (+ cess & surcharge)

TDS vs Actual Capital Gains Tax (Very Important)

Many NRIs believe that TDS deducted by the buyer is the final tax — this is incorrect.

TDS Rules:

20% TDS on LTCG

30% TDS on STCG

TDS is deducted on sale value, not profit

📌 Actual capital gains tax may be lower than TDS deducted.

👉 NRIs can claim refund or apply for lower TDS certificate.

🔗 This is explained in detail on our TDS on Property Sale by NRI page.

Exemptions Available to NRIs on Capital Gains

NRIs can legally save tax by reinvesting capital gains.

Section 54 – Investment in Residential Property

Applicable when a residential property is sold

Capital gains reinvested in another residential house in India

Purchase within 1 year before or 2 years after sale

Construction within 3 years

Section 54EC – Investment in Capital Gains Bonds

Investment in specified bonds

Lock-in period: 5 years

Maximum investment: ₹50 lakh

Useful when property reinvestment is not planned

Section 54F – Sale of Non-Residential Property

Applicable when selling land or commercial property

Reinvestment in one residential house

Strict conditions apply

📌 Choosing the wrong exemption can lead to full tax demand later.

Can NRIs Claim Refund of Excess TDS?

Yes. NRIs can:

File Income Tax Return (ITR) in India

Declare actual capital gains

Claim refund of excess TDS

This is very common when:

Property was held long-term

Indexation significantly reduces gains

Exemptions are claimed

Capital Gains Tax and Repatriation of Sale Proceeds

Tax compliance is mandatory before repatriation

Banks require:

Tax payment proof

Chartered Accountant certificate (Form 15CB)

Form 15CA filing

🔗 Read more on Repatriation of Sale Proceeds by NRI.

Common Mistakes NRIs Make

❌ Assuming TDS = final tax

❌ Not applying for lower TDS certificate

❌ Missing exemption timelines

❌ Not filing ITR in India

❌ Repatriating funds without tax planning

These mistakes often result in blocked funds or notices.

Do NRIs Need a Chartered Accountant?

In most cases — YES.

A CA helps with:

Correct capital gains computation

TDS optimization

Exemption planning

ITR filing & refund

Repatriation compliance

Early planning (before sale deed) saves the maximum tax.

Need Help With Capital Gains Tax Planning?

If you are an NRI planning to sell property in India or have already sold one, professional tax planning can save lakhs.

📞 9266032777 whatsapp /Contact

Get expert assistance with:

Capital gains computation

Exemption planning