phone

+91-9266032777

email

CaShiwalidagar@gmail.com

Calculate Capital Gains on Property in Delhi (2026 Guide)

How to Calculate Capital Gains on Property in Delhi (2026 Guide)

If you are selling property in Delhi, understanding how capital gains are calculated is essential to avoid paying excess tax or receiving an income tax notice.

Whether you are a resident or an NRI, the method of capital gains calculation determines how much tax you actually pay.

At CA Shiwali, South Delhi, we help property sellers accurately compute capital gains and legally reduce tax liability.

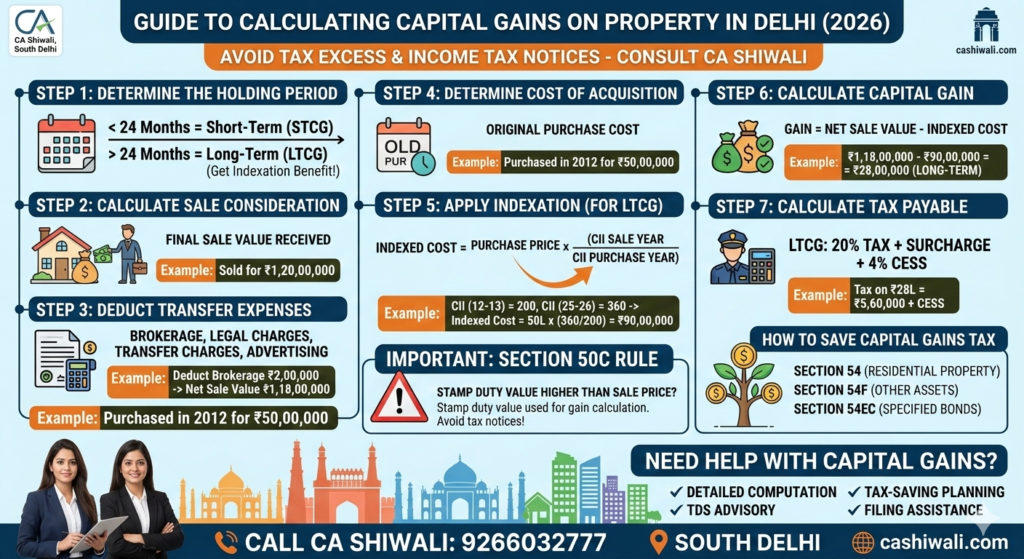

Step 1: Determine the Holding Period

Capital gains depend on how long you held the property.

Less than 24 months → Short-Term Capital Gain (STCG)

More than 24 months → Long-Term Capital Gain (LTCG)

Long-term gains qualify for indexation benefit.

Step 2: Calculate the Sale Consideration

This is the final sale value received from the buyer.

Example:

Property sold for ₹1,20,00,000.

Step 3: Deduct Transfer Expenses

You can deduct expenses directly related to the sale, such as:

Brokerage

Legal charges

Transfer charges

Advertising expenses

Example:

Brokerage = ₹2,00,000

Net Sale Value = ₹1,18,00,000

Step 4: Determine Cost of Acquisition

This is the original purchase cost of the property.

Example:

Property purchased in 2012 for ₹50,00,000.

Step 5: Apply Indexation (For Long-Term Capital Gains)

For long-term gains, indexation adjusts your purchase price for inflation.

Formula:

Indexed Cost = Purchase Price × (CII of Sale Year / CII of Purchase Year)

Example:

CII (2012-13) = 200

CII (2025-26) = 360

Indexed Cost =

50,00,000 × (360 / 200)

= ₹90,00,000

Step 6: Calculate Capital Gain

Capital Gain = Net Sale Value – Indexed Cost

₹1,18,00,000 – ₹90,00,000

= ₹28,00,000 (Long-Term Capital Gain)

Step 7: Calculate Tax Payable

For Long-Term Capital Gains:

20% tax

Plus surcharge (if applicable)

Plus 4% cess

Tax on ₹28,00,000 = ₹5,60,000 + cess

For Short-Term Capital Gains:

Taxed as per your income tax slab rate.

Important Section 50C Rule

If the stamp duty value is higher than the actual sale price, the stamp duty value may be considered for capital gains calculation.

This is one of the most common reasons for tax notices.

Common Mistakes in Capital Gains Calculation

Using wrong Cost Inflation Index (CII)

Ignoring improvement cost

Not deducting brokerage

Incorrect holding period calculation

Not considering Section 50C implications

Even small mistakes can result in excess tax payment or penalties.

How to Save Capital Gains Tax

You may claim exemptions under:

Section 54 – Reinvestment in residential property

Section 54F – Sale of asset other than house property

Section 54EC – Investment in specified bonds

Proper planning before selling property can significantly reduce tax liability.

Capital Gains Calculation for NRIs

NRIs must also consider:

Higher TDS deduction under Section 195

Repatriation rules

Form 15CA / 15CB compliance

Professional tax planning is strongly recommended before finalising the sale.

Frequently Asked Questions (FAQs)

1. How do I calculate capital gains on property sale?

Capital gains are calculated by subtracting indexed purchase cost and transfer expenses from the sale price. If the property is held for more than 24 months, indexation benefit applies.

2. What is the tax rate on long-term capital gains for property?

Long-term capital gains on property are taxed at 20% plus surcharge and 4% cess.

3. Is indexation mandatory?

Indexation is available only for long-term capital gains and helps reduce taxable profit by adjusting purchase cost for inflation.

4. What happens if stamp duty value is higher than sale price?

Under Section 50C, the stamp duty value may be considered as the sale value for capital gains calculation.

5. How can I reduce capital gains tax legally?

You can claim exemptions under Section 54, 54F, or invest in Section 54EC bonds within prescribed timelines.

6. Do NRIs pay different capital gains tax?

The capital gains tax rate is similar, but TDS deducted at the time of sale is higher for NRIs under Section 195.

Need Help Calculating Capital Gains?

✔ Detailed computation with indexation

✔ Tax-saving planning under Section 54 / 54EC

✔ TDS advisory for resident & NRI sellers

✔ Filing assistance and compliance

📞 Call Now: 9266032777

📍 South Delhi