phone

+91-9266032777

email

CaShiwalidagar@gmail.com

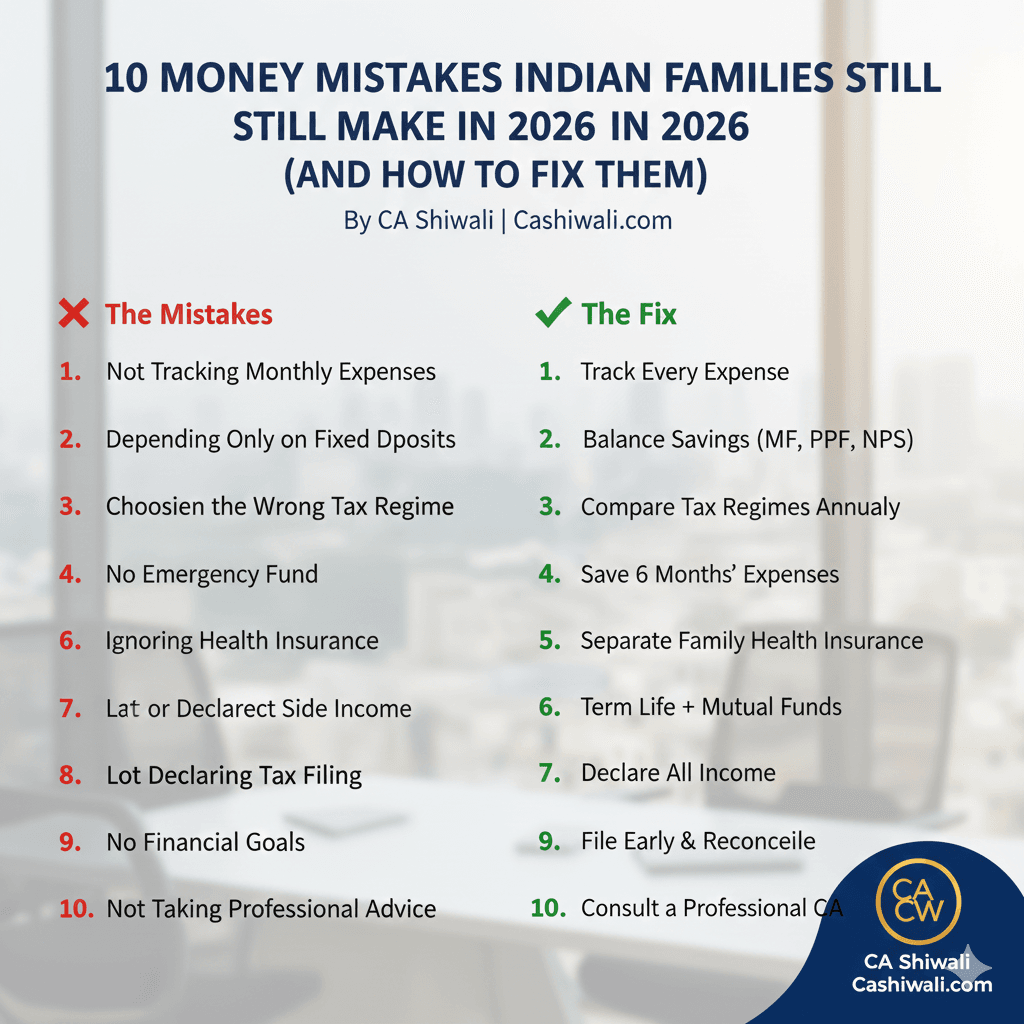

10 Money Mistakes Indian Families Still Make in 2026 (And How to Fix Them)

By CA Shiwali | Cashiwali.com

Managing money has become more complex in 2026. Despite higher incomes, better apps, and more awareness, many Indian families still struggle financially—not because they earn less, but because they make avoidable money mistakes.

As a practicing Chartered Accountant, I see these errors daily. The good news? Each one can be fixed with simple, practical steps.

Let’s break them down.

1️⃣ Not Tracking Monthly Expenses

Many families know their salary but don’t know where their money goes.

❌ The mistake:

No written budget

Relying on memory

Surprise expenses every month

✅ The fix:

Track every expense for 30 days using:

A simple Excel sheet

Google Sheets

Any basic expense app

👉 Awareness alone can improve savings by 15–20%.

2️⃣ Depending Only on Fixed Deposits

FDs feel safe—but they no longer beat inflation.

❌ The mistake:

All savings in FD

Ignoring long-term growth

✅ The fix:

Balance your savings:

Emergency fund → FD or savings account

Long-term goals → Mutual funds, PPF, NPS

💡 Safety is important, but growth is essential.

3️⃣ Choosing the Wrong Tax Regime

Many taxpayers blindly select the new or old tax regime.

❌ The mistake:

No tax comparison

No professional review

✅ The fix:

Every year, compare:

Salary structure

Deductions available

Long-term benefits

👉 The wrong choice can cost ₹50,000–₹1,50,000 extra tax.

4️⃣ No Emergency Fund

Life doesn’t warn before problems arrive.

❌ The mistake:

Zero emergency savings

Using credit cards for emergencies

✅ The fix:

Save 6 months of expenses in:

Savings account

Liquid mutual funds

This protects your investments and mental peace.

5️⃣ Ignoring Health Insurance

Medical inflation is rising faster than income.

❌ The mistake:

Relying only on employer insurance

Low coverage limits

✅ The fix:

Separate family health insurance

Minimum ₹10–15 lakh cover

Insurance is not an expense—it’s risk protection.

6️⃣ Mixing Insurance with Investment

Endowment and ULIP plans are still widely misused.

❌ The mistake:

Buying insurance to save tax

Expecting high returns from insurance

✅ The fix:

Term insurance for protection

Mutual funds for wealth creation

👉 Keep protection and investment separate.

7️⃣ Not Declaring Side Income

Freelancing, YouTube, rent, interest—everything is tracked now.

❌ The mistake:

Ignoring side income in ITR

Cash income not reported

✅ The fix:

Declare all income

Maintain basic records

In 2026, data matching is strong. Transparency saves trouble.

8️⃣ Late or Incorrect Tax Filing

Many people still file returns casually.

❌ The mistake:

Filing on the last day

Ignoring Form 26AS & AIS

✅ The fix:

File early

Reconcile income properly

Take professional help if unsure

This avoids notices, penalties, and stress.

9️⃣ No Financial Goals

Money without direction gets wasted.

❌ The mistake:

No clarity on future needs

Random investments

✅ The fix:

Define goals:

Child education

Home purchase

Retirement

Then invest purposefully, not emotionally.

🔟 Not Taking Professional Advice

Google and WhatsApp advice can be dangerous.

❌ The mistake:

Copying others’ strategies

No personalisation

✅ The fix:

Consult a professional who:

Understands your income

Knows tax laws

Plans long-term

A good CA saves more money than they charge.

✨ Final Thought

Financial success in 2026 is not about earning more—it’s about making smarter decisions.

If you avoid these mistakes, your money will work for you, not against you.

📞 Need Personal Financial Guidance?

Talk to CA Shiwali for:

Tax planning

Income tax notices

Salary & business structuring

Family financial planning

👉 Visit Cashiwali.com or book a consultation today.

Direct Consultation with CA Shiwali Dagar

Expert tax planning and compliance services tailored for NRIs, property owners, and businesses. Get professional clarity on your complex tax matters today.

Strategic Planning

- ✔ Capital Gains (Sec 54/54F)

- ✔ FMV Valuation (Pre-2001)

- ✔ NRI TDS & Form 13

Tax Compliance

- ✔ IT Notice Resolution

- ✔ 15CA & 15CB Certificates

- ✔ GST & Statutory Audits

Start Your Consultation

Whatspp CA Shiwali Now Call CA Shiwali nowProven Results. Online & Offline.